The reason I write the post is because I’m B&C shareholders and hope Nu becomes successful so that B&C can be finished in future, and also want to summarize my thought on stable private currency in these years.

A strong system demands less on the quality of its participants and a weak system demands highly on its operators. If Nu’s architect want same achievement as Satoshi’s bitcoin project, just imagine that the founder disappeared several years after the project’s launch, and the system still works fine.

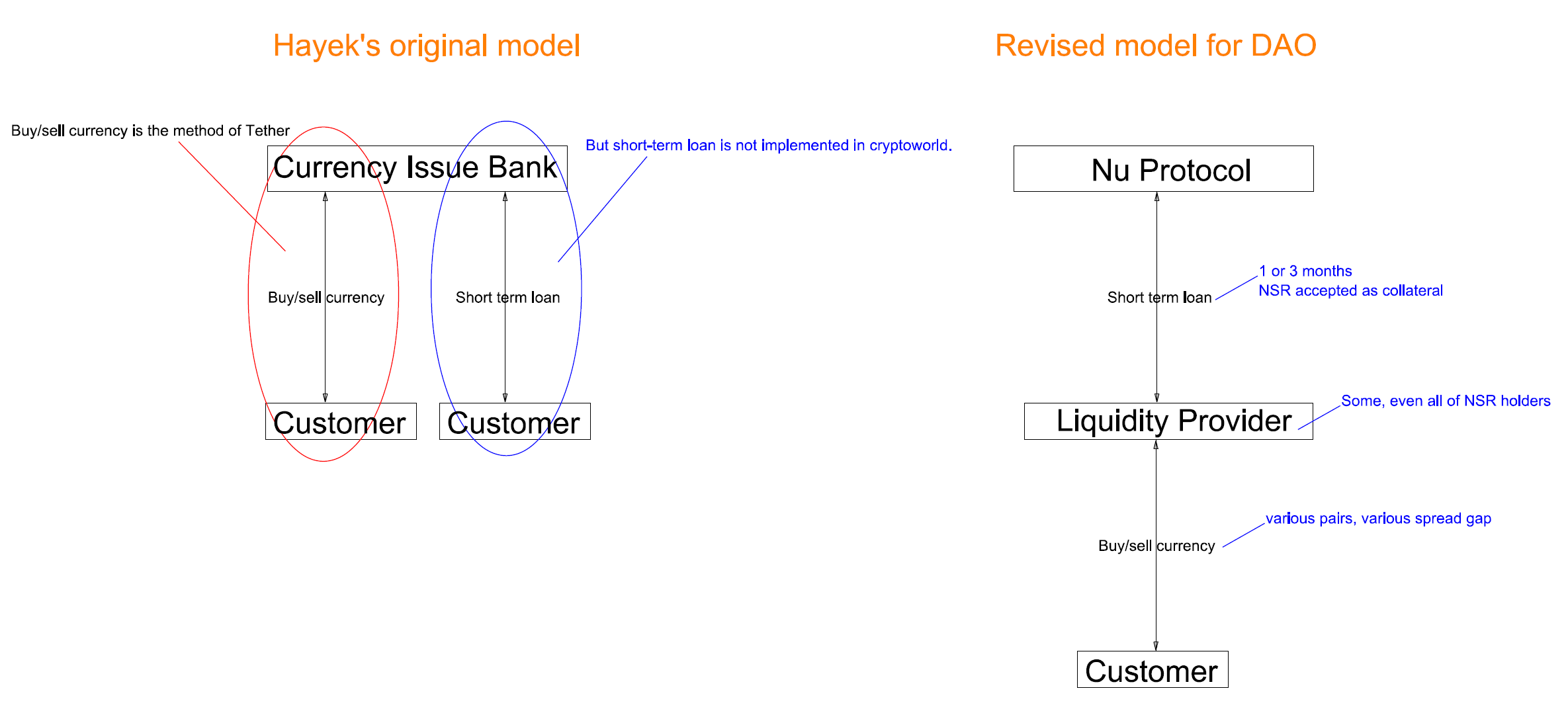

F. A. Hayek already told us how to issue a private currency, as per

https://www.mises.org/library/denationalisation-money-argument-refined

“The sale (over the counter or by auction) would initially be the chief form of issue of the new currency. After a regular market had established itself, it would normally be issued only in the course of ordinary banking business, i.e. through short-term loans.

”

Excerpt From: F. A. Hayek. “Denationalisation of Money: The Argument Refined.” iBooks.

If Nu’s “liquidity engine” becomes successful in future, we all be happy, but if it doesn’t, this Plan B is just for us to continue our effort. As per Nu’s liquidity engine, we sell NSR when NBT peg in danger and buy NSR when our reserve is high enough, the main purpose is to treat NSR market cap as a pool as we can input or output value when needed. The short coming of liquidity engine are:

- We have to build up a high liquidity market for NSR which is unnecessary while NBT’s liquidity is the only target.

- low value transfer efficiency due to price gap between buyback and sale of NSR.

- An infinite supply of NSR(at least looks like) will terrify&prevent potential investors(speculators) from buying NSR, therefore the liquidity engine may be out of fuel.

The Plan B is from the Nobel Prize winner’s short term lending mechanism which is immune to the flaw described above.

NSR holdes pledge their own NSR to borrow NBT from the protocol on a ratio voted on blockchain, then they provide liquidity for NBT. In this model, we shrink the NBT supply by manipulating the pledge ratio referencing the free market situation such as NBT demand, NSR price etc. The goodness are blow:

- Little expenditure, if NBT demand zero, NSR just become another “Peercoin”. Look at the BKS now, B&C is not finished, and BKC supply is zero, but BKS holders are minting. Sustainable!

If NBT supply is high, we don’t need to pay anything to LPs because they make their living by charging price spread fee as their income. Our customers pay for the service provided by LPs, fairness.

-

We don’t have to build up a high liquidity market for NSR on exchanges, and short term lending activity only occurs on Nu’s blockchain.

-

NSR is meant to be manipulated upwards just like BTC’s price plays important role in BTC’s ecosystem,

(To be revised.)

This post is about the currency model/mechanism, irrelevant to the inflation/deflation issue.

This post is about the currency model/mechanism, irrelevant to the inflation/deflation issue.

I guess at least 20X higher!

I guess at least 20X higher!

Of course C hates B.

Of course C hates B.