TL;DR

Better face some risk than spend $13k each month for an unreliable liqudity provision scheme

/TL;DR

Intro

In the past days I’ve spent an enormous amount of time and effort dealing with liquidity operations.

Now that the situation has a bit calmed down I thought about improvements.

I tried to identify what went good, what not so good and what even bad.

Findings

-

Arbitrage doesn’t work.

The inter exchange arbitrage doesn’t work. As long as a pool is below the target, there’s just no incentive to invest time and move funds to another exchange. Fixed cost might be able to mitigate that -

ALP aren’t reliable

Especially when liquidity is most needed, LP pull funds. I understand that. Better lose 0.24% per day than 15% from having the funds used to hedge the risk of others.

Once again, fixed cost might be able to mitigate that, but I doubt that the funds are sufficient to really keep the peg. -

The friction between the tiers is too high to move funds fast and efficient between them

-

NuBots in dual side mode can defend the peg

While I have no proof for it, I dare say the NuBots were very efficiently defending the peg, especially after all the iterations of tuning them.

I just don’t know what had happened without the NuBots being at Poloniex.

Would the trade have stopped, because the offers had been so far off?

Or would people have continued buying and selling NBT even at 10% offset? -

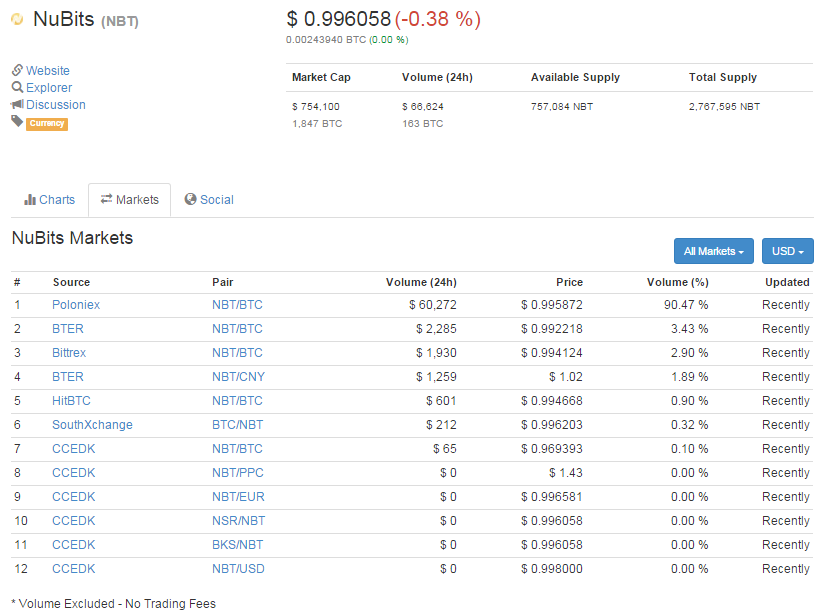

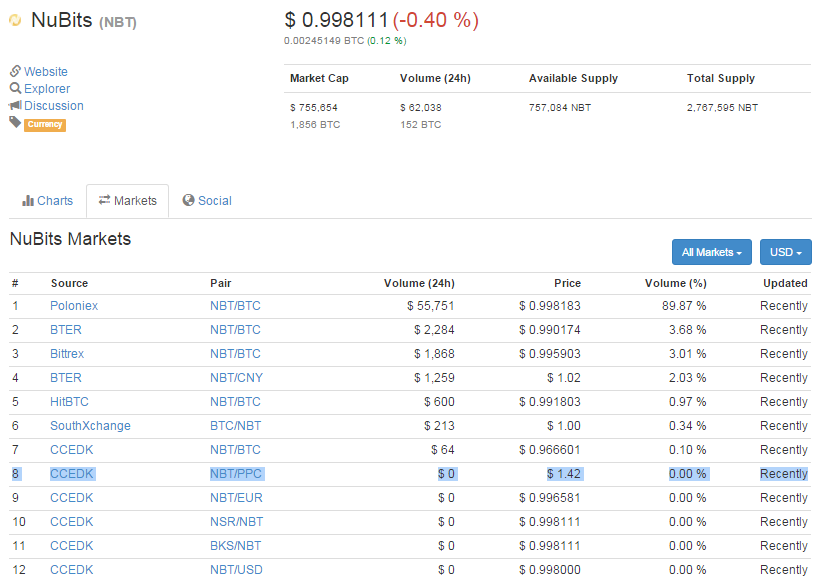

Current liquidity operation is exchange wise centralized

We need to face the truth that the current liquidity operation is de facto centralized. Trading happens on Poloniex.

We might support as many other exchanges with liquidity as we want and do, yet we can’t attract volume just by offering liquidity.

Users trade where the experience is superior, or the reliability, site design, etc. I have no clue

All I know is that offering liquidity alone doesn’t bring customers. -

Customers of the NBT/BTC pair are expensive

We can consider us lucky that not many more customers are active in the NBT/BTC pairs. Each time they successfully use NBT to hedge BTC volatility, Nu loses money. The risk for that was outsourced by the decentralized liquidity provision model; the costs aren’t. Nu needs to pay a compensation for that.

That’s an agreed upon status quo to advertize Nu and show the quality of Nu’s products. I have something in mind to improve that. Just hang in there!.

Exchanges and liquidity

The liquidity operations at so many exchanges costs a lot of money to compensate LPs for their risks. While it could potentially attract business, the lesson we learned from the recent quarters is, it doesn’t necessarily.

But still Nu pays a lot of money each month for LP who provide funds at exchanges with barely any trades. Unfortunately I have no historical information to prove that point, but the current status is here. 90% on on exchange.

Imagine how much money could be saved if Nu focussed on the exchanges where the business is!

Some might say that would lead to NBT being de-listed.

If so, I need to ask why?

There’s currently no trades even with liquidity support by Nu.

Considering that the ALP can’t be relied on especially when they are most needed, it looks like Nu wastes a lot of money for the cover-up, the illusion of providing liquidity

Keep hanging in there!

Paradigm shift - What if?

Imagine a radical change of liquidity operations.

At the moment each supported exchange gets buy side support and sell side support.

What if there were only some exchanges that buy NBT (hereafter: “major exchanges”), while there are a lot of exchanges selling NBT?

That might remind you of the gateways which I recently sacrificed for the greater good to let them be reborn as dual side NuBots.

Operating a sell side gateway is very little effort. NBT need to be deposited from time to time. The status can easily be monitored by the broadcast liquidity. BTC need to withdrawn frequently.

With this type of gateway you can support each exchange with a sell side. Not supporting a buy side (and announcing that long before doing it!) makes it so much easier.

The exchange(s) that offer buy side support might have ALP supported by Nu (I think they should) and are supported by a dual side NuBot.

If customers know - they need to be informed about that! - that they can buy NBT at many, many places, but sell them only at some, we can focus on the major exchanges.

That sounds like centralization, but it isn’t

It’s focus!

Each exchange that only has a gateway can be transformed into a dual side exchange in very little time.

If one of the major exchanges defaults and customers move to one that is currently only an “NBT selling exchange”, that can be changed soon. We move where the customers move.

Buy insurance or face the risk

One of the reasons why the liquidity provision has been transformed to a decentralized model, was the exchange default risk. A lot could be improved since then.

Back then there were hundreds of thousands of USD in NBT and BTC at exchanges ($70,000 jmiller; $300,000 kTm).

It looks like I could handle the recent Bitcoin roller-coaster with a total of between $40k and $50k of Nu funds.

If you add up all compensation that is being paid for ALP and MLP you have several thousand NBT each month (most recent grants):

NuPool 4,100

Liquidibits 2,200

NuPond 2,400

NuLagoon 4,700

That is over 13,000 NBT for liquidity operations.

If you put some tens of thousands at risk for some months without having the exchange default, you have a positive ROI.

Whenever that exchange defaults after those months passed, you are better off having provided liquidity with Nu funds than having paid for liquidity.

What if NBT can only be sold at Poloniex, NuLagoon Tube and Blocks & Chains Exchange once it’s finished, but bought at all exchanges which currently are supported by Nu?

The sell side only exchanges don’t need much funds. If they run dry, so be it! The marketing message needs to be clear: only dual side exchanges guarantee the peg!

Long-term insurance companies make the profit (if they calculate right). Nu buys insurance at LP who provide funds in ALP. They can calculate. They pull funds during roller-coasters - no offence intended, that’s the rational choice!

Executing the plan

Requirements:

- an army of RaPi2 or similar

- several “gateway custodians”

- a few “dual side custodians”

- Nu funds

- lots of marketing

- move funds to (FLOT or a subdivision of it, with 2-of-3 multisig and lesser funds) and from exchanges (custodians) regularly

Benefits:

- can save Nu an enormous amount of money

- makes liquidity provision more reliable

Drawbacks:

- non-crypto currency pairs can barely be supported by that. As the future of Nu’s liquidity provision is centred around BCE, this will only forestall that development

- the major exchange needs to survive long enough to reach a positive ROI (sell side only exchanges don’t hold an extended amount of funds)

- it’s unclear what impact comes from focusing on a few exchanges in regard to the trading volume there. I doubt it’s much different from now, but can’t say that for sure

{kind=link}

{kind=link}

{kind=link}