I disagree. The CCEDK operation/LiquidBits was setup to support some unique fiat pairs with liquidity. The intention is to allow users and traders to exit and enter through USD and EUR pairs. There is also a small wall (that has been reduced significantly lately) for NBT/BTC to cater for new users entering the market without fiat.

The cost is 10% of all liquidity operations, about 1k/month out of the 10k/month which I think is a reasonable deal. Bear in mind that the compensation on the fiat pairs is about 20-33% lower than for NBT/BTC pairs.

Especially on the EUR/NBT pair I’m seeing almost daily trades lately, which are typically users entering or exiting through fiat. Those are our core customers imo, to me the traders are secondary. It is indeed a bit disappointing to see that there is virtually no trading on the USD/NBT pair. Therefore I’m thinking of reducing that wall to be on par with the EUR/NBT if that continues to be the case. That will save some cost.

I do wonder what we get for the other 6-7k on NBT/BTC pools. Just a few Ks of volume and a loss for the LPs when Bitcoin is highly volatile. To me that is of diminishing value and at least 5k/month can be better spend on e.g. development.

Agree, the higher spreads during high volatility have proven to be effective. So we can reduce the ALP NBT/BTC walls and the cost on the NBT/BTC pairs imo. The peg can be successfully defended by NuBots as MoD has proven.

It will be Interesting to see NuPool’s next proposal. I suggest to allow some time to discuss it.

For them, supporting NBT/fiat will increase revenue (much) more via the volume brought by a stable crypto fiat such as nbt, than direct fees taken from nbt/fiat trading, I suspect.

This is why I was arguing for transforming the the liquidity provision scheme.

The current isn’t sustainable. It’s not scalable. It’s too expensive. It puts the peg we want to guarantee at risk, by fighting on so many fronts

In a hopefully not so far future, BCE can be the exchange for which Nu guarantees a more or less tight peg - both buy and sell side. The operation there will blur the lines between T4, T3, T2 and T1. Nu owned funds can be put on order at little risk there.

We are not yet there.

Meanwhile and maybe even then, NuLagoon Tube can be one of the “official exchanges” with supported dual side operation.

We need to focus on a limited number of exchanges, otherwise we might lose that fight for the peg.

Wanna sustain a NuBot operation at every exchange to support the peg?

Too expensive!

Wanna rely solely on ALP for the most exchanges?

Too expensive - if it damages the so far flawless brand image!

Again, this is no centralization. We can do out business at any exchange. We focus to improve our products!

We arrive there better, cheaper, with less danger for the peg

if we stop supporting the buy side at so many exchanges

focus on buy side at the exchange(s) with the major trading volume

support these exchanges with ALP and dual side NuBots (Nu funded)

convert all other exchanges to sell side only operations (with no guarantee for a sell side peg!)

follow the customers, move the dual side operations where the customers move

in case the customers move the trade to a formerly sell side only exchange

convert the NuBot to dual side

increase the NuBot funds there

ramp up ALP there

limit the efforts to not burn out people, who are involved in liquidity operations

If I speak of NuBot, I mean NuBots, ideally with different operators.

Sell stamps anywhere - buy them only back at a guaranteed price at selected places! Keep the peg at those places. Care less for the other places.

That even brings Nu in the position to make deal with exchanges - as long as they have volume and stay dual side, the exchanges make a lot of money (the trade volume is the reason for Nu to support them; the CMC price is a weighted average!). Ask for a reduced fee for NuBot operator accounts!

@Cybnate

IMO - NBT/USD isn’t used as much on CCEDK because it is more difficult, expensive and time consuming to withdraw to a USD bank account than it is a Euro/SEPA bank account.

Not so sure about that. We need some exposure. A trading pair without volume will be removed from the exchange. It is not that we are trading on 100s of exchanges, there are just a handful. I think we need to make sure people can find us across a number of exchanges, especially when on one of them e.g. defaults occur.

This can be reduced significantly but not to zero I believe. We need to move slowly as this can create some shocks on the sell side as LPs might sell their NBT when no longer being able to obtain rewards on ALPs.

I must admit that I liked the concept that basically everyone could anonymously provide liquidity by running a bot without bothering too much about market technicalities and sharing in the rewards for providing it. It is a pity that we are losing this model and moving back to a small group of core LPs or NuBot facilitators, but I do see the high cost of sustaining the current ALP model.

Switching to NuBot sell side only will not remove all trading there. It can be used to limit Nu’ responsibility for the peg if properly advertized.

Arbitragers will operate the buy side - supposedly quite successful most of the time.

If people want to get their NBT traded for BTC, they need to go to a “certified” exchange.

This increases Nu’s ability of keeping the peg, because fewer exchanges need a lot of attention, while reducing the efforts (time, money) of it.

This will stay true - but not for all exchanges!

ALP with CRFB is very useful to provide funds on T1.1, while the NuBots will operate on T1.2 and T2.

So there’s still need for people who run bots anonymously, etc.

We aren’t going to lose that model. We are moving forward and make the best of both worlds the next iteration of the liquidity provision scheme.

This will likely not be final. BCE will offer the chance for the next iteration by vastly reducing the friction between T4, T3, T2 and T1(.1/.2).

I consider my proposal an immense improvement. Otherwise I wouldn’t have spent so much time trying to put the essence of my experience in words.

Again, this is just my vision.

I might be wrong, but I think I’ve provided an analysis why the current scheme needs improvement and made some points about how to improve it.

Add to it:

advertize that change and make sure, customers know about the “limited warranty” for peg on all small exchanges. I wouldn’t even guarantee a sell price for NBT. If the NBT are sold and not refilled, the sell side might end up without peg as well.

The reason for this is simple: you don’t want to have a lot of Nu funds there.

Depositing and withdrawing funds should rather be scheduled actions (e.g. weekly) than on demand.

If you don’t have to care for a lot of exchanges, you can focus on the important ones (which might change over time). The important ones are those on which you act according to demand.

You can’t herd cats.

There is also a very low chance that we loose the peg on those pairs. I’m not too worried about that.

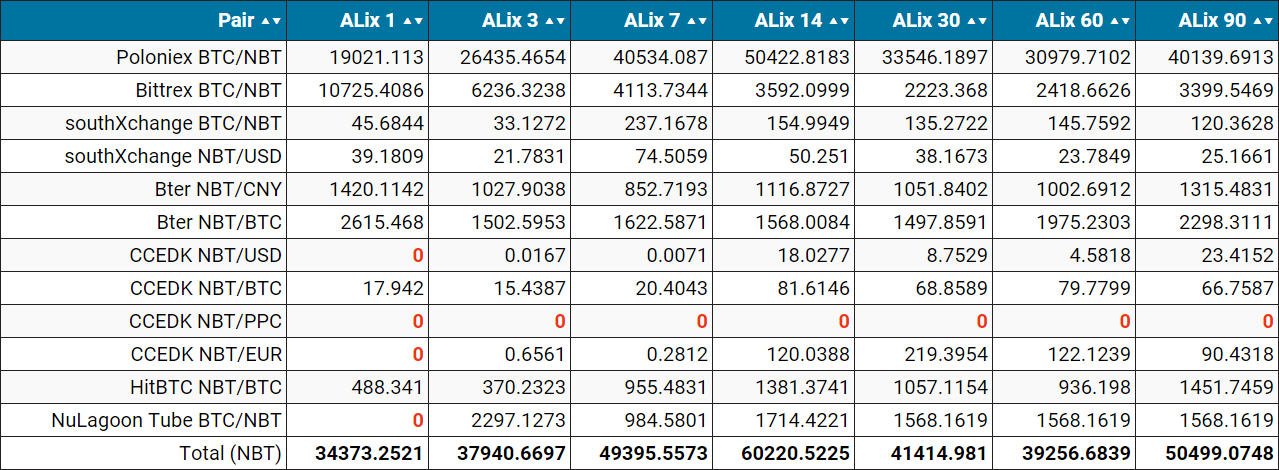

Except for the NBT/PPC pair which is not supported all pairs are being traded on from time to time. I would just keep them on Alix so we can monitor any changes.

Somebody who wants to make a point can do it easily.

“Breaking” the peg on not fully supported exchanges would be no issue, do no harm, if the message of Nu would be clear:

peg enforced at selected exchanges; buy and sell NBT there at close to $1

NBT sale at a lot more exchanges - without guarantee for peg; NBT will be refilled regularly, but may run dry in between

Do you really think sustaining liquidity operations at all exchanges, which list NBT, is possible?

We have to select/focus anyway.

Let’s draw consequences to the benefit of Nu and start focussing!

…it’s hardly possible to keep Poloniex under control…

Double dare you. Give me your money, I beg of you.

But still, the point stands, it’s one thing to allow arbitrage channels to buy NBT for less than a dollar when it feels downward force while it’s entirely another to actively provide buy side support at exchanges.

The best point you can make is to simply empty one side of an ALP and notice that it takes near infinite time for it to rebalance.

Maybe it’s necessary to explain explicitly at what danger the peg is due to the inefficient liquidity provision scheme.

An attack can be done like this:

look for an exchange listed on CMC that has little volume and a few orders (maybe some ALP funds, because it’s “supported” by Nu)

buy orders on both sides to the degree to which you want to move the peg

start trading with yourself

pay nothing but the exchange fee for that

create $100k volume for $200 fee

derail the peg

Applaud to yourself for having done what others couldn’t do.

In addition to the fees this costs nothing more but the removal of the buy and sell side orders, which stand in your way.

For that reason you choose an exchange with low trading volume and not too many volume on order.

Try that at an exchange with NuBots that have $30k funds available which can be put on T1.2 and T2, an exchange that is monitored, etc.

It’s possible, but way more expensive.

Find a balance between the risk of funds at the exchange and the risk of an attack.

Hope for a soon arrival of BCE and have a buffer of $100k or more to be put on parametric order book.

Aren’t you afraid of evil competitors, who don’t shy away from such an attack? Or fanboys of competitors?

Do we really have to get hit hard, before we understand it doesn’t work this way?

How are you doing that? I can make a 10 cent transaction at $1 to make CMC read $1 again. Are you putting up sell orders at under $1? In that case, thanks for the free money, I have T3 funds I can leverage.

You will bee too late and I will have made tens of thousands of USD volume.

Isn’t the display on CMC the weighted average?

Is it really only the last price?

Still the CMC chart would look ugly in between the attack and your “peg restoration”.

I’m not talking about a globally lost peg, just a local and limited (in time) event.

Still a lot of potential for bad publicity.

An attacker with malicious intents will avertize it afterwards…

Why do we want to keep that attack vector and pay a lot of money on top for it?

Does that make sense?

Asymmetric pools at least save close to 50% of the compensation.

Single side NBT gateways are even cheaper.

I think I stop here.

I’ve written enough about it.

As a LP and a share holder, I don’t mind moving this direction.

Go where the liquidity is.

I would nominate - Polo, Bittrex and BTER

People will have to step up to man the NBT sell gateways though. And they can’t charge high fees - or it would just be cheaper to run the ALP. One person should probably run a few exchanges.

Why cant we just do alp sell side only and cut liquidity costs in half? That’s why i ask why not do something like a 10:1 sell:buy split, so there’s at least a little motivation to clear away orders <$1 other than just the arbitrage opportunity.

I think @masterOfDisaster 's rationale is convincing overall.

Maybe we should first drastically reduce the operations on exchanges that have near zero volume and see the reaction from the market for 30 days.

Then if there is no issue, completely cut off the liquidity over there subsequently.

It’s possible but not very probable. Once people start to notice cheap nubits exist the attacker’s money is on the line due to the very visibility he makes.