Is it possible to sort the exchanges by trading volume rather than total volume of orders on the book - at least as another option?

It’s hard to track liquidity on the exchanges with lots of volume (which might be more important in terms of peg perception) as soon as sides start to run dry.

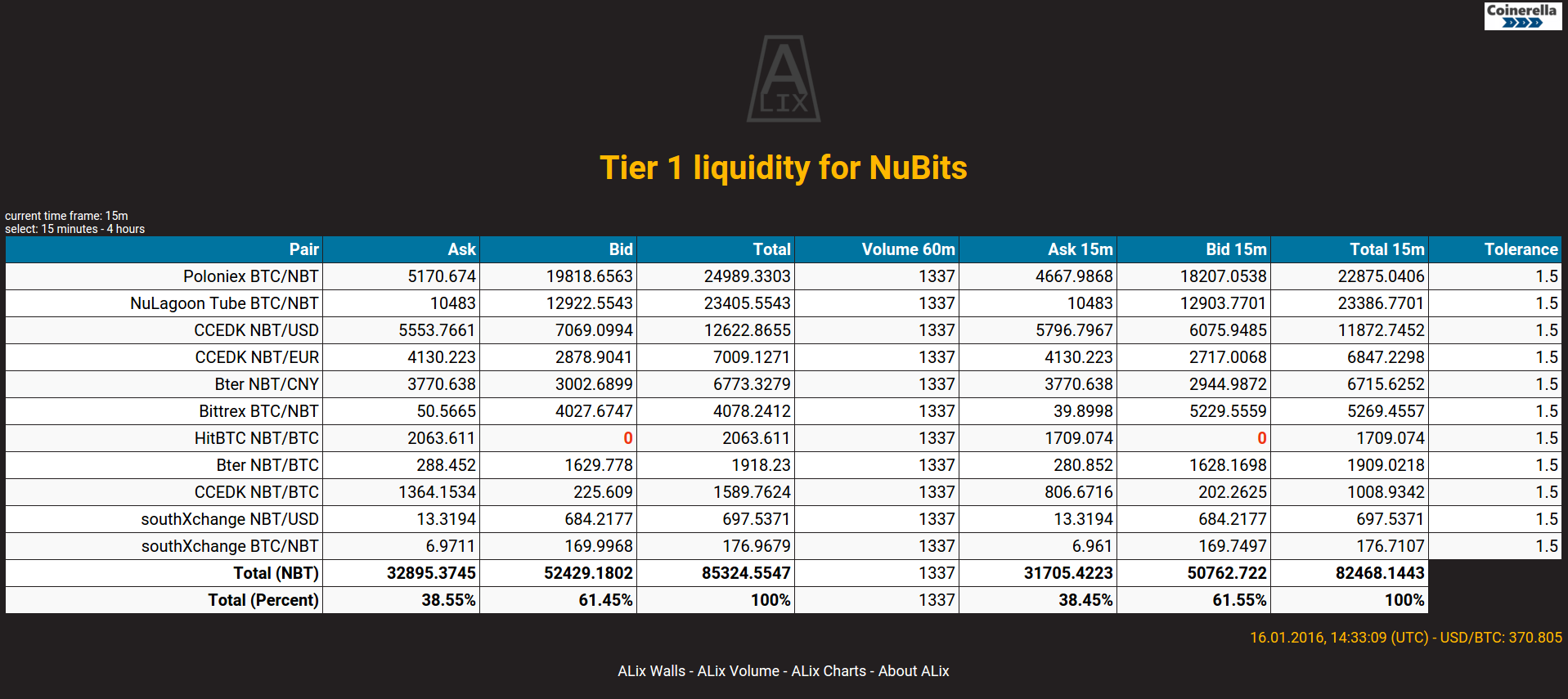

Or to say it in a more simple way:

I’d like to have Poloniex on the first row; at least as long as most of thr trading volume is there.

Last 30-60 minutes trading volume

Reasoning: the exchange with (recently) the most trading volume is in biggest danger to run dry at one side or another rather sooner than later.

Without trading volume, the walls just remain where they are, unless LPs pull funds.

In fact the total trading volume is less important than the ratio between traded volume and available volume.

I’m not gathering that data yet, so it would be a little more work for me (I will have to touch every single exchange wrapper and add the trade history), but I think it will be worth it.

As for the UI, I think I’ll put it right between the current ALix Walls and the MA data.

Like this:

I hope it makes sense.

Before you spend a lot of efforts on it, I’d like to know what others think.

Would that improve the quality of information and provide us with useful data to make better predictions about the need for interventions?

NuLagoonTube gets counted twice on ALIX volume because of rebalances (which are economic certainties in the Nu world). [In my opinion this is because NuLagoonTube is T3 and not comparable to other T1 volumes]

A T3 address will count all deposits and withdrawals as ‘Transactions’. In T1 only the withdrawals matter, and basically the exchange adds another pseudo-layer to differentiate and report trade volumes independent of what goes on with the addresses on the back end.

We could add in something like that pseudo-layer by ignoring all deposits and withdrawals that come from FLOT, JL, or NuLagoon addresses. Then the only thing missing from NuLagoonTube being real T1 liquidity at that point is independent verification from a third party. For example, if this pseudo-layer is in place then theoretically NuLagoon can deposit or withdraw to the address and choose whether to register the volume or not. So they could do something like sell to an unknown address, transfer to NuLagoonTube, and buy off the books, then sell again. This would cause infinite sell volume, and basically just shows that NuLagoon can do anything they want as far as reporting trade volume once the pseudo-layer is in place. That’s why independent 3rd party verification between an exchange, a pool operator, and Nu is important for calling it T1 liquidity.

An exchange finds two people that want to trade and matches them up, making a single trade. NuLagoonTube acts as a middle man, making an exchange with one party and then the other at separate times, counting it as 2 trades. So in the situation where person A wants to buy 1000 NBT and person B wants to sell 1000 NBT at the same time, the total volume would be 2,000 NBT in NuLagoonTube and 1,000 NBT in a normal exchange.

So, to paraphrase that: Either @henry would have to start filtering the 24h volume or ALix would need to do that in order to have representative volume?

I mean, ultimately they’re apples and oranges because of the middle man effect as opposed to the maker/taker relationship. However, ignoring rebalances from FLOT, JL and NuLagoon itself would certainly ho a long way.

?

?