Motto

It’s early for this motion, but it’s never too early to (try to) improve things.

tl;dr

Using T6 buy side (NSR) to refill T4 buy side (BTC) over time is more efficient than dropping NSR at the market only after BTC funds have been depleted.

The same thinking is the reason why NSR buybacks are conducted over some time and not at once.

Plus it makes handling easier and actions more clear if T4 and T6 don’t interact with T1-3 independently.

The current motions that are up for voting (@JordanLee’s version and @Nagalim’s version) both start selling NSR to support the peg if all T4 buy side funds (BTC) are depleted. This is less efficient to defend the peg compared to what I’m going to propose.

I have adjusted a lot more parameters to tie T4 and T6 close to each other, trying to make the job of the FLOT more efficient. The FLOT should be guided by thresholds and triggered actions instead of being left to discretion and the need to start discussions what to do, when and how.

This is dangerous especially if the peg is under pressure!

You might read the background information and my reasoning below or fast forward to the motion draft at the end (before the appendix).

Intro

I was almost begging your pardon for this post because of the length of it. I couldn’t have written it much more compact except for leaving out the explanations why I propose this and that the way I do it.

So honestly, I’m not feeling sorry for this wall of text - I consider it necessary to give you more than just the results.

If you are bothered by it, simply ignore it. I just try to contribute as good as I can.

The development of rules, actions, triggers is very important if Nu wants to evolve, if Nu wants to solve the puzzle of being a distributed corporation that needs to delegate some power to people who fulfil roles, because the protocol sometimes might just be too slow for the market.

Warning

NSR holders be aware that the FLOT executes your will based on motions and only uses discretion if situations arise that are not reflected in the terms of operation!

It is in your responsibility to refine the terms and adjust thresholds and values based on experience and effectiveness of the current terms!

The marrow

So here’s an adjusted version of the motion that aims at governing the actions of the FLOT as well as the recommendations for NSR holders. It’s based on a mix of @JordanLee’s version and @Nagalim’s version, but it’s heavily altered.

A lot of my adjustments is based on what I wrote in “Interpretation of the liquidity tiers, a waterfall model, triggers, metrics and actions”. That thread deals with more than T4 and T6, but includes them of course.

I was hoping to spark a discussion with that thread but failed. So there’s a lot more in my head that didn’t find its way into that thread (there was just no reason to write it down), but is included in this thread.

Here’s some explanation of the adjustments I made, because I didn’t want to put it in the motion text. It doesn’t belong there, but I find the reasoning important, because it makes it easier for readers to get to their own conclusion if they know why I came to mine.

Regarding BTC

I don’t how to treat non-BTC/non-NSR buy side funds. If NBT are ever sold for anything but BTC or NSR (I wonder how…), this currency could be converted to BTC (as long as NSR are not much more liquid), because it makes accounting easier and saves the FLOT from managing different types of multi signature addresses, run different clients, etc.

I decided to adjust the related T4 buy side and T6 sell side terms to “Nu products will only be sold for BTC or NSR”.

I moved BTC related terms to the top.

Although I hope that in the future selling NSR will be preferred over selling BTC to remove NBT from the market (and to vastly reduce the BTC funds), this requires a much more mature NSR market with more liquidity and for the time being selling BTC needs to be the first measure to support the NBT buy side.

I increased the threshold to which the buy side shall be filled, because the FLOT actions might be less agile than the market and I expect filling the buy side to only to 40% provides not enough buffer in case an additional purchase is required. The FLOT is faster than Nu motions or votes, but still takes some time.

The total USD value should rather be dynamic than static. If the total amount of NBT in the wild increases, the buffer needs to increase as well.

I calculated 12% of the total value of NBT in the wild as 80,000/(4,731,444 (total NBT) - 4,040,000 (FSRT funds) - 100,000 (recent development grant not yet in the wild)). I have no clue how much funds are granted, but not (yet) in the wild.

And I’m not sure whether it’s a good idea to exclude the development grants from the calculation, because sooner or later they will be in the wild…

The idea to take a percentage instead of a fixed amount tries to take into account that a dynamic buffer provides more security for the peg. I think keeping it dynamic is useful for some time.

The buffer needs to be filled if consumed by supporting the buy side or to compensate BTC volatility.

I was planning to speak of “products” and not NBT, but I think for now “NBT” is fine; CH-NBT, EU-NBT, X-NBT will take some time before they are launched. As soon as there are different types of products, this draft might need some more adjustments (like increased T6).

I don’t like Nu paying the price for BTC volatility at this place as well (in addition to the costs for compensating liquidity), but as the buy side liquidity is of utmost importance for the peg, Nu’s credibility and Nu’s success, I wouldn’t dare to gamble with that. Selling NSR to increase the amount of BTC (keeping it at a minimum level) sounds strange, but is necessary to ensure a safe and sound peg.

If the price of BTC drops by far and that leads to a reduced value of funds in T4 it’s necessary to prop them up, because as soon as BTC starts rising, people will want to sell NBT for BTC. If the T1-3 buy side funds run dry, T4 buy side support is required. Better not have the T4 buy side funds depleted by that!

But don’t worry - I’ve put a buffer into this before NSR sale kicks in and fills T4 buy side. It should really only be triggered if necessary (T4 needs to be down to 75% of its target).

That means at the moment 25% of $80,000 = $20,000 in BTC would already have been used to support the buy side. I don’t want to see Nu continually buy and sell NSR unless there’s much more liquidity, but I think this is a condition under which selling NSR to receive BTC seems to be appropriate.

With a current T1-3 liquidity1 of in total approximately $150,000 ($145,541) moving buy side from 35% to 45% requires less than $15,000 and more importantly less than $20,000. The first triggered T4 buy side action doesn’t trigger T6 buy side action based on current numbers. If T4 buy side action gets triggered a second time, it might be required to start selling NSR to support the peg by refilling the T4 buffer.

T6 buy side could be used directly to support the peg, but I consider management easier the way I proposed it.

As my T4 buy side is designed to be dynamic in relation to the NBT in the wild, it hopefully stays this way - NSR sale only triggered if buy side needs to be supported by T4 repeatedly.

If you let T6 and T4 act with T1-3 independently, you might overshoot the mark. Using T6 to fill T4 prevents that.

In case the value of T4 rises above a threshold, wealth needs to be distributed. Currently there’s a motion in place to conduct share buybacks. That is for the time being the preferred approach amongst a majority of NSR holders. If not, the motion wouldn’t have passed.

I was thinking about distributing T4 funds and different periods of time (e.g. 12 hours vs. 48 hours) for the triggered actions to refill T4 or distribute T4 funds, because I want to have T4 funds refilled quite soon if they start to run dry, but don’t want to trigger an action to distribute funds too early in case of a not lasting BTC upwards price swing.

As I didn’t want to mess up with current motions to conduct share buybacks, I didn’t include this, but think it could be useful for future versions:

-

If the ratio of BTC value in T4 buy side exceeds 15% (average) for more than 48 hours, a distribution of the funds in excess is triggered.

The details for that distribution are based on a separate motion and are not part of this motion.

This way a separate motion could deal with the distribution of the funds as soon as the threshold for distributing them based on this motion is reached,

This motion would define when (in a conditional sense) while another motion would define what to do.

If Nu were to sell additional products it might be appropriate to distribute dividends as well, because the low liquidity of the NSR market would lead to buybacks for months unless Nu wants to create a bubble by pumping a lot of value into the market in a short period of time…

I think that a part of that wealth needs to be distributed more quickly to get rid of the volatile BTC that are held in excess. Dividends are an option to do that.

As this is a very controversial topic, I’d rather have that defined in a separate motion.

Regarding NSR

I raised the amount of NSR on multi signature addresses, because in difference to BTC, NSR held in an address pose no risk for Nu except for the risk of theft - I sincerely hope that this is successfully mitigated by an appropriate choice of n-of-m multi signatures.

Assuming that the NSR reserve were at 6% of total NSR, this would mean 6% of 831,636,146 (at the time of writing) or almost 50 million NSR would be held in T6 buy side.

This sounds like an impressive amount, and indeed it is. But considering the liquidity of the NSR market, I doubt that even 10% of the 50 million NSR could be sold for BTC (or NBT) in a short time without having a significant impact on the NSR price.

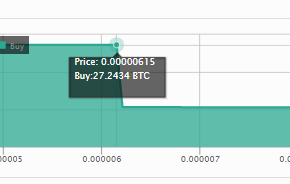

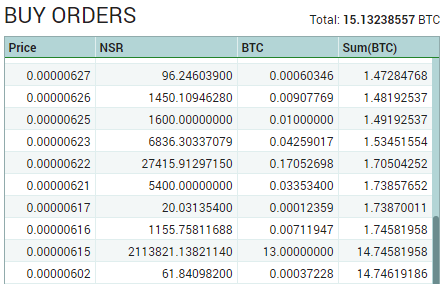

With less than 100,000 NSR you could push the NSR price at Poloniex down to 615 Satoshis2 and only because the buyback has put a wall there. At bter it’s similar, but requires close to 1,000,000 until the NSR buyback wall is being hit3.

Trying to sell 5 million NSR would erase most buy orders on Poloniex and bter combined - and these are the top exchanges with over 90% of daily trading volume!

That’s why I’d rather fill the T4 buy side (that might be consumed by buy side support; if T4 is below some threshold) by selling NSR over time than wait until T4 is depleted to start a panic sale of NSR.

Even if you ignored the effect of selling NSR on market price and multiplied the amount of NSR with the current rates of BTC/NSR and USD/BTC, you would end up with

50,000,000 NSR * 0.000009 BTC/NSR * 380 USD/BTC = 166,500 USD.

This is not that much, if you try to include the effect of the sale of a huge amount of NSR on the market value. Especially if you think about the reason for this buffer, you might want to have a sufficient buffer - it takes time for an NSR grant to pass.

Having NSR in a multi signature address poses no volatility risk!

One might wonder whether it makes sense to have that big a buffer if it’s doubted that the NSR can be sold at reasonable prices. If that’s the case, Nu is close to failing anyway, because it won’t be able to grant NSR fast enough. It doesn’t hurt to have a bigger buffer in that case anyway.

T4 and T6 combined has not enough value to buy every second NBT in the wild back. I can’t say I like that ratio, but hope for the T6 buffer to be sufficient until NSR grants could refill it. And most of all I hope that Nu is on the way to rather expand NBT supply than contract it - who knows; better be prepared!

I already mentioned it in the “BTC” section - as soon as there are additional types of products, the percentage of NSR in T6 needs to be increased; to what level is subject of another iteration of this draft.

Regarding NBT

Once again increased buffers. Reasoning like at NSR.

Having NBT in a multi signature address poses no volatility risk!

This motion draft doesn’t deal with a static value (x NBT), but a dynamic value (y% of NBT in the wild) that adjusts to an increased supply. This is assuming NBT could go viral and increasing the buffer doesn’t have much of a drawback, but a benefit of a better chance to keep the peg in that direction as well - at least I suppose that the risk of increasing the amounts is successfully mitigated and so I expect to have only the benefit of an increased buffer left.

The 20% of NBT in the wild are close to 120,000 NBT. This is somewhere in between what Nagalim and JordanLee proposed in their versions.

Considering that additional 150,000 NBT will be available through the FSRT (according to this motion here), this is (FSRT and FLOT combined) roughly half of the current supply of NBT in the wild. This should give enough time for NSR holders to grant additional funds in case the T4 sell side runs dry. I don’t expect that an inflation by more than 50% of the current NBT in the wild is required in only a few days.

Last remarks

I was close to declaring the FSRT the “T6 sell side” and introduce the FLOT as “T4 sell side”.

But then I thought what I already wrote (this prologue and the draft that follows) is confusing enough.

Still I hope some people take their the time to discuss this.

I sincerely believe that sooner or later a motion that heads into this direction needs to replace the motions (@JordanLee’s version and @Nagalim’s version) which are currently being voted on.

One reason is that the FLOT should operate based on terms that are as precise as possible rather than on discretion.

Would NSR holders really feel comfortable with the fate of Nu (hence the property of the NSR holders!) in the hands of a few people that might discuss rather than act?

If there’s no rule, there needs to be discussion. A majority of FLOT and FSRT members needs to agree on a course if not defined by the terms of a motion.

I urge you to discuss about rules now instead of leaving that up to a few people (FLOT, FSRT) who’d be better off executing than discussing.

I very much hope that the motion is consistent in itself, but need to admit that I got tired towards the end, writing, tuning, checking it (the thresholds, the triggered actions), trying to prevent oscillation while tying the tiers 4 and 6 close to each other.

The motion draft

=##=##=##=##=##=## Motion hash starts with this line ##=##=##=##=##=##=

BTC - T4 buy side

All T4 buy side funds shall be transferred to a multisig address shared by this group.

The total amount of BTC in this multisig address shall be 12% of the total value of NBT in the wild.

The introduction of additional products (CH-NBT, EU-NBT, X-NBT) will be included in a future motion.

Rules for use of BTC or other T4 buy side funds:

-

BTC will be used to purchase NBT when the buy side funds falls below a 4 hour average of 35% of total liquidity in tiers 1, 2 and 3 for NBT. The amount of purchased NBT is calculated to restore the buy side to 45%.

-

The NBT proceeds will be placed in the T6 sell side multisig currency address controlled by FLOT.

-

FLOT will be bound by the same rules established by shareholder motion to conduct share buybacks in cooperation with @NSRBuyback.

NSR - T6 buy side

Existing T6 buy side funds shall be transferred to a multisig address owned by the First Liquidity Operations Team, FLOT.

6% of the total NSR supply shall be granted to this address.

It’s strongly recommended that NSR holders grant additional NSR if the FLOT multisig address contains less than 4% of the total NSR supply no matter whether that’s due to an increased total number of NSR or consumed NSR funds.

Rules for use of NSR:

-

If the ratio of BTC value in T4 buy side falls below 9% (at average) for more than 12 hours it shall be filled to 10% by NSR sales within less than 48 hours and to 12% in less than 168 hours after the threshold was reached.

If the buy side falls below 9% before it was filled to 12%, a new loop starts: T4 buy side shall be filled to 10% by NSR sales within less than 48 hours and to 12% in less than 168 hours after the threshold was reached.

The reasons for the drop of ratio of BTC funds can be BTC volatility or NBT sale; this won’t be treated differently. -

Additional details about how much to sell, how much at a time, etc should be determined by the signers in real time, because much more information will be available at that time than shareholders have now. The Nu network is confident in any course of action agreed upon by the required majority of the signers.

-

If the ratio of NSR in the multisig address owned by the FLOT exceeds 8% of the total NSR supply, the funds in excess get burned and the transaction ID gets publicly listed.

-

If previous motions for conducting NSR sales conflict with the rules presented in this motion, they will become invalid. However, signers should look to previous auctions as an example of how future sales might be conducted.

NBT - T6 sell side

The introduction of additional products (CH-NBT, EU-NBT, X-NBT) will be included in a future motion.

20% of NBT in the wild shall be granted to a FLOT multisig address.

It’s strongly recommended that NSR holders grant additional NBT to fill the funds up to 20% if the FLOT multisig address contains less than 15% of the total NBT supply.

The First Strategic Reserve Team (FSRT) will continue functioning as a backup to sell side pressure provided by this group. FSRT has a total of 4,040,000 currently in its possession. Any funds the FSRT has in excess of 151,500 NBT should be burned within 14 days of when the NBT grant to FLOT is made. No commission or compensation will be paid for funds burned.

Of this 151,500 NBT, 1% (1,500 NBT) is allocated for compensation to members of FSRT like previously agreed to.

Rules for use of NBT:

-

If sell side liquidity in tiers 1, 2 and 3 for NBT drops below a 4 hour average of 35% of total liquidity, the FLOT shall sell NBT in the open market until the sell side is restored to at least 45% of total liquidity.

-

If the ratio of NBT in the multisig address owned by the FLOT exceeds 25% of the total NBT supply, the funds in excess get burned and the transaction ID gets publicly listed.

-

NBT will only be sold for BTC or NSR. Other currencies aren’t allowed to purchase NBT.

-

BTC proceeds of NBT sale shall be added to T4 buy side funds, stored in the according FLOT multisig address. Rules for T4 buy side apply then to the funds.

-

NSR proceeds of NBT sale conceptually shall be added to T4 buy side funds.

NSR received for sold NBT are directly transferred to the T6 buy side multisig address of the FLOT instead (bypassing T4 buy side FLOT address) to save from meaningless transactions.

General rules

The preceding should be interpreted as guidelines, and FLOT may exercise discretion if situations arise that are not covered by the terms above. Communications between FLOT members regarding decisions on how to use funds must be publicly visible.

In order to form FLOT, at least 3 signers must be selected by motion. Additional signers will be accepted for a period of 14 days after this motion is passed.

=##=##=##=##=##=## Motion hash ends with this line ##=##=##=##=##=##=

Appendix

1 - NBT liquidity

date

Mon Nov 9 20:28:27 UTC 2015

nud getliquidityinfo B

{

"total" : {

"buy" : 80312.1137,

"sell" : 65229.8596

},

"tier" : {

"1" : {

"buy" : 23960.8717,

"sell" : 22807.4773

},

"2" : {

"buy" : 10027.38,

"sell" : 6026.687

},

"3" : {

"buy" : 37225.3736,

"sell" : 31380.0

}

},2 - NSR/BTC at Poloniex:

3 - NSR/BTC at bter: