BTC is very stable recently. I recognise that there is a risk of high volatility due to the uncertainties of the block halving though. The ALPs should be more flexible with that. I believe we had that discussion before.

I believe there are three possible reasons to justify the decrease in liquidity over the last months:

- the provision of generous liquidity at a tight spread was perceived as not so much rewarding for nubits sales

- the perhaps mistaken anticipation that b&c will decrease drastically the costs of liquidity which gave a psychological incentive to underestimate the importance of a tight spread

- the fact that it seems that the peg was saved back in january by the trememdous efforts of mod via the gateways which demonstrated their value; then it seems that there has been a consensus that gateways are very cost effective

I agree that we should keep a tight spread with a large liquidity but at the same time it costs Nu a lot, it seems.

Perhaps even if we reduce drastically the rewards for liquidity provision we will attract a large participation from liquidity providers.

Anything that points to that phenomenon? To me it is not obvious at all.

PS: maybe @JordanLee wants us to take more risks. Maybe he wants us to basically increase liquidity at the cost of printing a lot of NSRs to maintain the peg. Maybe as a startup we should do that.

But then we need to know when we got to do some nbt sales. Recently we sold 30k on a single day. At the end of last year we sold 100k in 2 days. Maybe providing a generous liquidity as a tight spread will create a lots of nbt sales that would counterbalance the sales of nsr to keep the peg.

Nu proved that it can do that and shows that it can handle daily volumes of above 3,000,000 NBT:

Providing a big amount of liquidity at a very tight spread increases the costs by far compared to using a parametric order book.

This is what the current liquidity provision - at least at Poloniex - looks like; even in an extended version.

There we have

- ALP (NuPool) providing liquidity at a quite tight spead

- MLP (NuLagoon) supporting liquidity on a tight spread while being independent from liquidity providers who might pull orders at the blink of an eye

- NuBot/PyBot operations at an increased spread to provide a line of defence if the prior fail; the NuBots start with orders at an increased spread and have parametric order book enabled on top

With Nu funded operations this can be much lower - if the funds don’t get lost.

I come back at Poloniex where a mix of Nu funded operations (NuBot/PyBot) and Nu paid operations (NuPool, NuLagoon) tried to combine the best of both worlds.

Long term Nu funded operations are cheaper. But they have the ongoing risk of loss of funds.

If that stays true for the coming months, we should ramp down ALP and focus on Nu funded operations.

That’d save approx. ~8% monthly (cost of ALP: liquidity costs plus operator fees) while making 1% revenue.

9% monthly is an APR of close to 200% (including compound interest).

Break-even would be in a few months. Poloniex just musn’t go bust in that time ![]()

Reworking NuPool to use ALPv2 took time. It reduced the liquidity. But high liquidity at exchanges is a showcase and not more.

It earns Nu no money to have NBT traded at exchanges; on the conrary: it costs Nu money to support that.

It’s not the best of times to wish for an increased liquidity at exchanges (and not only because of the approaching Bitcoin coinbase reward halving and the expected effects on BTC volatility!).

The reserves are quite low.

The rule set how to replenish them is under construction (e.g. with “Core and Standard” motion).

The risk when providing liquidity with Nu funds due to echange default, theft, etc. is higher than it will be with B&C Exchange.

Buying liquidity through ALP is costly.

I’d like to see Nu operating in a conservative mode for some more months. Nu isn’t in the position to operate at full throttle.

Even if Nu would spend much more for ALP to attract liquidity, it couldn’t provide an appropriate backup, last line of defence for a big liquidity through Nu funded liquidity operations (NuBot/PyBot) for a big liquidity at the moment. There arene’t enough BTC for that!

My strong advice is to keep acting consevratively until B&C Exchange is working (or a surge of NBT demand fills the reserves).

Focus on the exchanges where the most liquidity is (at the moment Poloniex).

Keep a tight peg there with a few thousand USD on orders at T1.1 (ALP/MLP).

Have some more thousand USD on T1.2 (NuBot (including parametric order book)/PyBot)

I’ve never tried to fight that. I was a strong opponent of restricted network access and I’m completely on the side of having liquidity at a tight spread.

But I argue for limiting that amount at a tight spread at the same time.

Liquidity at a tight spread is expensive.

Nu can’t afford to have tens of thousands of USD value at a tight spread; not at the moment. And what for? To prove that it can do that? Nu already did.

If you want to do that again, ramp up ALP and/or fill accounts of NuBots with Nu funds. Both costs Nu money.

Let’s keep a low profile until B&C Exchange is ready and you can provide liquidity on T1.1 and T1.2 (with parametric order book!) with funds that currently sit on T4 while having no exchange default risk and only a very, very low risk of theft (which is, if B&C Exchange works as deisgne almost 0).

I agree with most of that.

There needs to be liquidity.

But having no sane limit for that liquidity is just as much suicide as having no liquidity is.

Nu needs a sufficient amount of liquidity at a tight spread.

Beyond that amount, higher spreads are justified.

Nu can’t support all exchanges with liquidity.

Focussing on the most important exchanges (NuLagoon Tube and Poloniex at the moment?) is crucial.

1 Like

my 2 satoshis as a non shareholder:

I used to play with nupool for a while, but the reward did not outweigh the risks, so I stopped doing that: providing liquidity.

If you want more liquidity nupool should pay out more for the providers, not less. It is simple economics 101.

1 Like

Thank you for providing feedback, which is very valuable!

It underlines the assessment that the tighter the spread is, the higher the resulting cost is.

The tightest liquidty (ALP) comes at the biggest costs. For that reason it needs to be limited to a reasonable amount.

Allowing an increased spread at the same compensation level would lead to the same result (more liquidity).

At the moment additional liquidity (additional to NuPool) is provided by alternative solutions (NuLagoon, Nu funded NuBots) and I think in total the liquidity is in good shape at Poloniex.

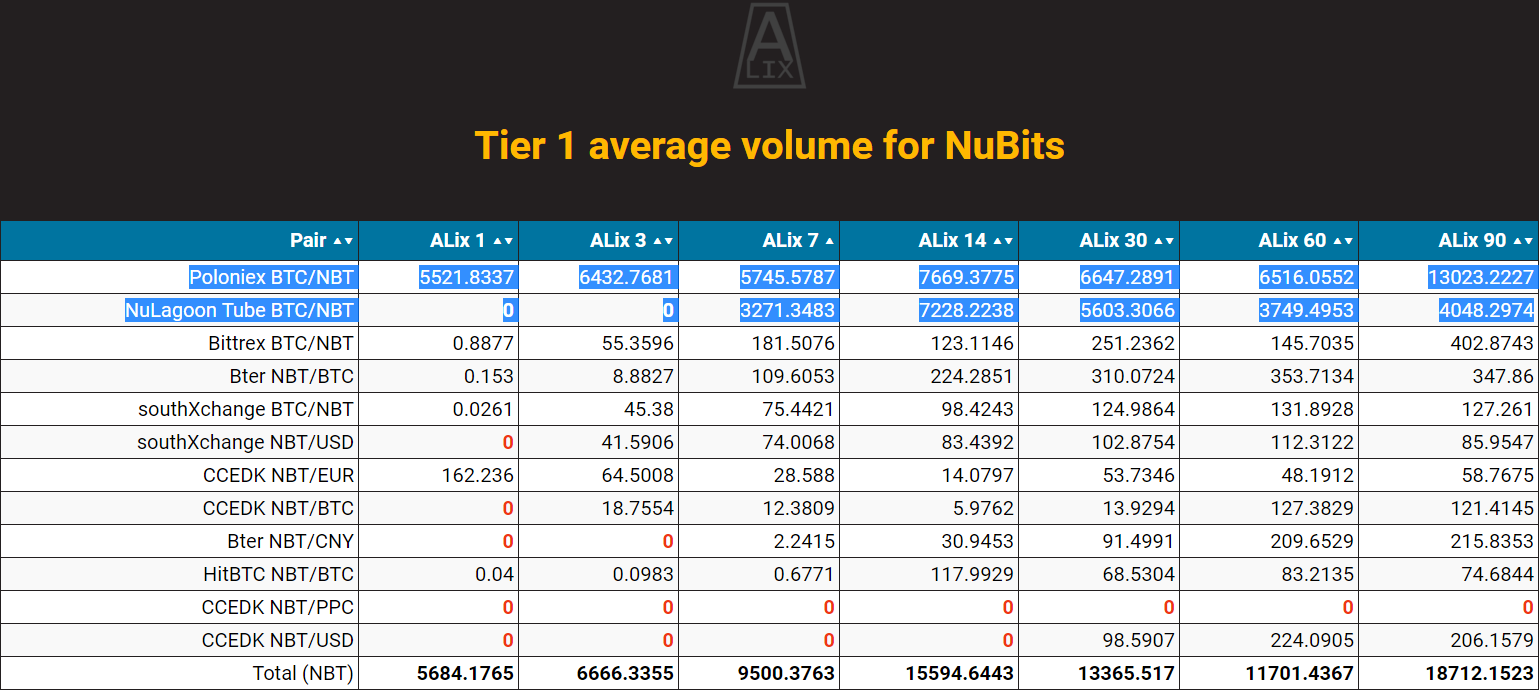

Liquidity network wide is a different matter, but obviously the liquidity provision is currently centered around Poloniex and NuLagoon Tube (ALix T1 volume sorted by 7 day average):

I think this is an oversimplification. There are a lot of things going on, including several pretty serious technical issues with clients and services.

So you unilaterally reject all attempts at RNA?

We have a motion for this, but I agree there needs to be another. Basically, the statement is 2%, rather than 1%. Anyway, it’s what basically everyone is running on. ALix grabs within 1.5% offset, which is a 3% spread, but most pools are running with ~1% tolerance. That means we buy at $0.99 and sell at $1.01, which I think is fine for most purposes. The market and moving bots and many LPs and all that helps to close the spread. Further renditions of NuBot will also help.

However, to equate spread with our current biggest threat is not something I agree with. We’re doing fine on spread. Liquidity magnitude and consistency is what we need to work on. And fees? Why even bring that up in the context of current threats? Fees have never been different from the starting values for any substantial length of time.

1 Like

Yes, a tight spread should be maintained regardless of the level of BTC volatility. I don’t accept the notion that speculators know which direction the price of BTC will go, which suggests liquidity providers will have their profits increase during times of BTC volatility, because there will be more volume from which to make the half percent profit that occurs each time NBT is sold at 1.005 or bought at 0.995.

A tight spread during times of BTC volatility will invite speculators and people hedging BTC to purchase NuBits. The proceeds of these sales will be used for NSR buybacks and increase the NSR price.

While we have a long term goal of providing a stable and liquid currency ideal for all kinds of business, right now we need to understand our market consists almost entirely of cryptoasset traders who will use NuBits as the cash portion of their portfolio and to hedge a decline in BTC or ETH. We have to win in this small market before we can expect to have the strength and size to win in other currency markets.

4 Likes

I’m glad to hear this.

minus exchange fees, deposit/withdraw fees to rebalance, NuLagoonTube spread, opportunity cost, etc. We can put the dev costs and FLOT costs and stuff on NBT increasing in supply, sure, but we have to account for an LP’s total perspective. We can’t just blind ourselves to what they actually have to experience to keep liquidity up for Nu.

Neither I

I agree that BTC halving is actually a very good chance for us to promote NuBits

Absolutely.

It is unnecessary to raise fees to support the peg, and planning to do so will certainly have a negative impact on NuBit adoption. It is exactly the sort of thing that I would characterize as a suicidal tendency.

BTC price can’t be accurately predicted but

- The latency in price updates can give brief but definite opportunities of arbitrage

- Speculation is partly a self-fulfulling prophecy, in the sense there’s a non-trivial correlation between BTC price drop and collective belief of such occurence. Due to uncertainties this can’t be gamed easily by individual traders, but I believe Nu loses money to them as a whole. It is thus paradoxical to offer NBT primarily as a hedging instrument.

My opinion is that tight spreads can be a loss-leader if we have a proper platform to collect fees by offering loans and derivatives. Without that it’s a money losing business.

It is an important question whether arbitrageurs are draining value from the liquidity providers. I doubt this is occurring. Muchogusto’s experiment is giving us interesting data on this. Unfortunately, the data set is too small to reach a conclusion, but I think it does indicate any losses that might exist are not very extreme. Muchogusto was all in NBT for the main upswing in BTC during the experiment, although the experiment has made smaller gains by being in NBT on smaller declines and in BTC on smaller gains.

But let’s consider the details of how arbitrage works. Prices at various exchanges don’t move synchronously. At a particular moment there may be whale wanting to buy BTC at Bitfinex immediately, with price being a secondary concern to that whale. He may push the price up at Bitfinex a percent. This prompts an arbitrageur to sell BTC at Bitfinex and buy BTC with NuBits at Poloniex, thereby buying low and selling high simultaneously in different markets. This action does not produce a loss for the NuBit liquidity provider. He makes a profit on the spread and the arbitraguer makes his spread as well. It is the whale on Bitfinex who is paying the cost to get what he wants right now. In a sense he is the loser, but in another sense he is not a loser either because he got what he wanted when he wanted it, he just paid an extra fee for the convenience. Arbitraguers are our friends and can make the network profitable in this way. They are in the business of giving impatient traders who pay a premium what they want right when they want it. It these impatient traders who take the loss, or pay an extra fee for their trade.

yes, money come from moving

1 Like

A worse scenario is that NuBot is too slow to update a price change and this is caught by an arbitrage bot.

Say BTC/USD is currently 450. A sudden drop occurs in many other exchanges to 440, but NuBot has to be stuck at buying BTC with 450 NBT for 30 seconds. I dump 1 BTC for approx 450 NBT (minus fees), and wait for NuBot to change its price, and repurchase 1 BTC with approx 440 NBT. The liquidity provider lost money.

I’ve been seeing that walls are consumed more quickly than I can react (the reversed price display on Polo definitely doesn’t help) during large price changes, prompting me to consider an actual risk that this is done by some people in the wild.

Now that I think of it, this isn’t called arbitrage, but is a problem buried within the messy details of ALP.

5 Likes

NuLagoon are advocators of Best Liquidity. we will write a formal response in other thread.

That indeed is a problem of NuBot, because it bets before speculators. However, that problem is overcomed by NuLagoon Tube due to the completely different design. In tube, the trading price is determined after the “Tube-in” transaction captured by NuLagoon in the blockchain. In other words, we let speculators bet first and give them a fair price.

I don’t think anything in my RNA proposal was poorly disguised - it is quite obviously a default mechanism. Shareholders continue to ignore contingency planning for a scenario where 90% of NuBits demand evaporates overnight. Default preparations are not a standard part of our operations; it is an end-game plan to preserve the network. To avoid these preparations is irresponsible.

If there are 1,000,000 NBT worth of currency demand today, and only 100,000 NBT worth of currency demanded tomorrow after a permanent crisis event (such as a government declaring it will prosecute anyone who holds NBT), it doesn’t matter how tight we keep our spread. Some NBT users must lose USD value of their holdings.

My RNA proposal attempted to add a semblance of fairness by providing a differentiation mechanism to ensure those who are willing to pay the most to redeem their NBT do so. The alternative to RNA in my permanent crisis scenario is at least a temporary collapse in the peg, and possibly permanent if no speculators arrive to purchase NBT.

I wholeheartedly believe in tight spreads and high liquidity in regular operations, as there is no question it improves the value of NuShares. I also believe in having a plan for a disaster situation. My RNA proposal is still the only mechanism that would preserve a 1.00 USD peg for users (provided they wait until the emergency state is lifted, which could be days, weeks or months as available supply reduces to match demand) in the event of a complete demand collapse. It is a common mistake to confuse continuing operations with crisis planning, and nothing in this post addresses the second concept.

2 Likes

We would like to share our understanding of liquidity operation and what it means to NuBits

A stable decentralized currency should have enormous demand. We believe only the case that people want to transfer money freely and to hold liquid asset anonymously could generate thousands times of NuBits current circulation. Then, why we don’t see those demands come? Just simply because people don’t 100% believe they can cash out their NuBits for Dollars for any amount and any point of time.

A few month after NuBits launched, I began my role of liquidity provider with my own money. I remember I not only asked for a high compensation, but also raised a special request. I requested my money was less than 20% of the total LPC liquidity size. Because I didn’t really believe I can 100% get my money fully back in future. But if there are 10,000 in liquidity operation, I tend to think the chance to cash out my 2,000 NBT in short term is high. I guess there must be lots of people have similar ideas.

That leads to the conclusions we would like to draw:

-

The more liquidity the better confidence people will have on NuBits. If the daily trading volume is 10k, 100k fund on liquidity wall is NOT waste of money. For example, 80k fund on the Tube walls doesn’t have any trades in last three days, but we don’t treat it as a waste, we even want to add more fund into the walls if we have more. Because those money can just simply sit there to give critical confidence to people on their holding on NuBits. “Hey, we have plenty money to cash out your NuBits”

-

The guaranteed duration of liquidity is crucial. Although I can cash out 10k NuBits in the 100k liquidity wall easily today, I have no idea on what it will be in one month or in one year. I still not comfortable to store my money which needs to be spent in a few months in NuBits. Imagine if there are 1000 BTC are guaranteed to sell for NuBits at the price $1 for 1 month, 500 BTC guaranteed for 2 month, and 200 BTC guaranteed for 6 months. I will be very comfortable to hold 10k NuBits for 3 months, and it is high possible to hold another 3 months when I found NuBits is in a good liquidity shape in 3 months.

However, guaranteed duration is much more expensive than tight spread. Liquidity provider will ask for much higher compensation. The innovation in NuLagoon ETP(exchange-traded pool) is to address this issue. In ETP, there are two exit doors for pool investors, one is redemption, another one is to sell on exchanges. The latter one will become the most liquid one and major one when the exchange is established. If BearBTC/BullBTC is sold on exchanges, the buyers money will replace their share in ETP, leaving the size of money in ETP and the size of money in liquidity operation not changed. That is a significant value point, resulting we could extend the ETP’s close period while doesn’t negatively affect the liquidity in pool investors’ respective. Therefore we can reduce the cost for locking the funds in liquidity operation for a guaranteed period of time. This mechanism is original from exchange-traded close-end fund, which can lock a certain amount of fund for a few years while provide very good liquidity in exchanges. It is a very mature idea and already been proved work well.

7 Likes

I have made a proposal to decrease the spread on my ~20,000 in liquidity to 0.5% from 1%. Please read and comment.