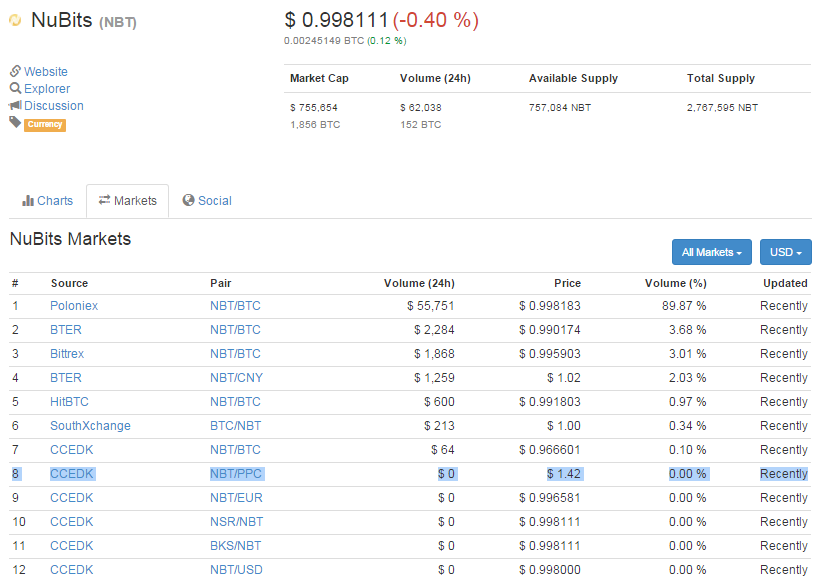

Just as any other trading pair is, if there’s volume. The drawback of (?-)NBT trading pairs is that they are most likely not being used to trade back and forth and rather to exit or entry fiat. That reduces the fee an exchange can collect with that.

If an exchange already has done all what’s required to be connected to the fiat system, a NBT/fiat trading pair is just extra profit.

I’m still struggling to understand why it isn’t obvious, how close Nu might have been to a disaster in the past week and why the proposal I made, isn’t perceived as the mitigation it might be.

Maybe I explained it the wrong way. Bear with me, I’m still recovering. What I write might not be as structured as it should be.

Please allow me to explain the concept of “major exchanges” with dual side NuBots combined with fixed cost ALP to reduce costs and improve reliability in greater detail.

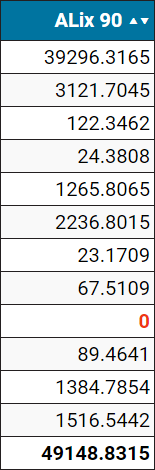

Unfortunately the awesome new ALix feature to display nupool ALP funds over time has no data for the past 7 days to show how low the ALP funds were on Poloniex.

@willy, @woolly_sammoth: is it possible to have an anonymized overview of the rewards of nupool participants who provided liquidity over the last 7 days at Poloniex? A total (and not per anonymized participant) reward would be fine as well. It’s only about deriving the average volume at the sides from 2016-01-15 (00:00 UTC) to 2016-01-21 (00:00 UTC) - during the most recent Bitcoin roller-coaster time!

Having the payouts per minute put into a graph would be neat. If I have the raw data, I can try myself!

I hope this can be useful to prove two points:

- fixed cost alp needs to come, because the current scheme failed (that seems to be non-controversial)

- a combination of fixed cost ALP and Nu funded NuBots can be more efficient than the current setup (I still believe it was more or less the dual side NuBots that kept the peg in the last 6-7 days) with only ALP (or MLP) supporting the peg

- fixed cost ALPs reduce the amount of money that needs to be kept at exchange (for the NuBots), because it improves the reliability of the first line of defence. The current NuBots rarely had a working first line of defence. Still it was sufficient to prevent the peg from failing totally. Total funds on exchange to achieve that: $40k - $50k.

- NuBots in the second line of defence require no immense first line of defence (big ALP volume for which a big compensation needs to be paid).

I expect the fixed cost ALP to be a viable first line of defence (operating on T1.1; in the linked post referred to as T1))!

The NuBots will be a second line of defence (operating on T1.2 and T2; T1.1 in the linked post referred to as T1*) with a higher offset, that is sufficient to support the peg while making Nu money from the offset, if the first line fails (temporarily) and traders buy into the NuBot walls.

I’m leaning on those divergent definitions (“T1.1” and “T1.2” instead of “T1” and “T1*”), because they will likely find their way with that naming into NuBot.

I suppose a permanent funding of approximately $15k to $20k (compared to a total of $400k that was kept at exchanges in total during jmiller and kTm times!) can provide a sufficient second line to buy time to deposit funds, if the first line is permanently so low that the funds on the second line start to get drained/traded.

Fixed cost ALP can be run with lower (total) compensation than the current ALP, because you literally only use it as buffer and require not such a big target to have that buffer working.

Being in the front line still is worthwhile for ALP, because the fewer funds on order book, the higher the reward percentage.

As long as NuLagoon Tube and T3 custodians have funds, fixed cost participants will trade funds to grab a piece of the reward. ALP will keep funds ready that can be put on order fast (T2) and will likely keep funds on T3 to buffer demand on the order book. They will trade with T3 custodians (or NuLagoon Tube), after they have first filled the low side (time is money), relaxing the situation for the peg and the T3 custodians.

If T3 custodians aren’t requested for making trades to fill T1.1, they may decide to fill T1.2, if that defence layer starts to run dry. That buys time for FLOT to refill T3 custodian funds AND exchange accounts if need be.

This is speaking about drastic change of demand, which we already faced several times in the last weeks and especially grave in the past 7 days.

And with the reduced amount of funds Nu needs to hold on exchange (compared to now with a totally failed first line of defense) the risk is significantly reduced.

Overall the cost of liquidity provision is reduced while the peg is supported more reliably.

As a ball-park figure, I guess Poloniex can be sufficiently supported with $2k to $3k per month. Operating dual side NuBots (yes, we need more than just one: redundancy, multiple operators, increased combined withdrawal amount, etc.) is little work - if they are really just passively operated and the operator only needs to keep them running and withdrawing exceeds.

Refilling low sides will be done from ALP first (T1.1), if that fails or takes too long, T3 custodians can help directly (depositing into T2, that gets automatically promoted to T1.2) and if that isn’t sufficient, FLOT can be activated (T4).

Can you see the beauty of that?

This can finally put the work on more shoulders and increases the reliability doing that!

Maybe the numbers might convince you.

Current monthly cost/risk analysis for liquidity provision:

Cost

Funds at risk

- Nu: $0

- ALP (Poloniex only): up to $40k if targets are reached; other exchange come on top!

Future monthly cost/risk analysis for liquidity provision:

Cost

- $4k ($2k - $3k for Poloniex + compensation for gateways)

Funds at risk:

- Nu:

- $15k-$20k (Poloniex)

- $10k-$15k (gateways)

- ALP: maybe $10k - $15k? (only at Poloniex required)

I left out costs for T3 custodians, NuLagoon Tube, etc. as they need to be paid anyway.

If Poloniex doesn’t default within 4 months after this scheme gets implemented, Nu is at positive ROI (a failing “gateway” exchange ha little impact)

And please don’t tell me a that defaulting Poloniex with both (current) ALP sides ($40k ALP funds in total) had no price that Nu needs to pay beyond the compensation that is already being paid.

I might explain the single side NuBot (aka gateway) scheme in a later post, although I think that one is quite clear.

Operating a single side NuBot is very little work if the operator doesn’t need to care about the funding.

{kind=link}

{kind=link}