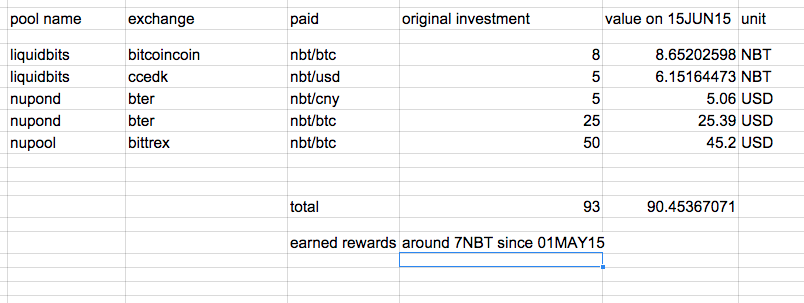

I put 93NBT as seed money 1.5m ago and the value of my fund on 15JUN15 is estimated to be 90.5 USD at current CNY and BTC prices against USD.

I earned roughly 7NBT as rewards.

So in the end, I am in the black: +4.5 NBT.

This is 3.22% monthly return.

Not bad.

But I am not sure if I was lucky or not.

Also, from Nu’s perspective, what was the value produced by such a liquidity provision?

Financially speaking, it is obviously a pure loss since I do not think we issued new NBTs in the mean time.

One way to nullify that loss or to drastically reduce that loss is to make the traders that use NBTs pay for that liquidity provision service.

That is why I think we need urgently to impose a higher minimum spread as I started to talk about here and as it is mentioned here by @dysconnect and then the needed custodial grants for liquidity provision can be reduced.

Some people like strict pegging of NBT, and dislike spread(0.95 -1.05 $).

My suggestion is to experiment loose pegging with BKC, reasons below:

BKC is just used to pay transaction fee on B&C, we don’t have to bother ourseleves with strict pegging, just relative stable(eg .0.9-1.1$). As long as transaction fee is cheaper than traditional exchanges, customers don’t care about 0.1% or 0.11% fee, do they?

Although BKS holders may vote to strict pegging.,we can avoid compete with NBT at least temporarily, both USD and post stamps backed by same US goverment, but BKC and NBT backed by different companies (DAC) because in future the intersection of NSR / BKS holders is unknow.

We offer different spread options such as 1% to 10%. Let BKC liquid providers select which is the their favorite, they may select 10% spread (0.9$ buy wall -1.1$ sell wall,big profit room) but other providers with 2% spread always trade firstly, so in the end, the market reaches equilibrium, free competition free market.

When bitcoin price flcutuates violently, most providers will choose 10% even 20%(0.8-1.2$) pegging, that’s fine because in that speculation environment, most customers don’t care about the small 20% fee change*(0.1% or 0.12% ), they’ve already got a lot profit or lost a lot.

In this way, BKC liquid providers get profit with the spread, B&C DAC’s expenditure is ZERO. BTW, B&C collects transaction fee from LTC/BTC, Doge/BTC pairs etc, therefore B&C becomes low spending high profit company.

I don’t think we’re providing any bkc liquidity. I think it just stays value at $1 cause that’s what it’s worth when you use it to trade on B&C. I could be completely wrong though.

Custodial grants of BlockCredits should be given to custodians for the sole purpose of placing sell walls and using the proceeds to distribute Bitcoin dividends.

…

In any case they should always be sold for one US dollar. While BlockCredits are the same as NuBits to the code base, they have a completely different purpose. They are solely for use as transaction fees and are not intended for general trade as NuBits are. Accordingly, a peg for BlockCredits will not be maintained. They are comparable to postage stamps in many ways. They are sold with the promise you will receive one US dollar worth of transactions on the B&C Exchange. Just as you wouldn’t expect to be able to sell postage stamps to a third party at face value, there shouldn’t be an expectation that BlockCredits can be sold for one US dollar, although a resale market may appear. BlockCredits should only be purchased with the intent of consuming them to pay transaction fees on the B&C Exchange.

This is part of why I think the business design of B&C Exchange’s operations is potentially lucrative. The single largest cost to shareholders (maintaining a peg) is eliminated. All BlockCredit sales are pure profit.

In order to trade crypto on B&C, people buy some BKC in advance, after some time, they find BKC on their hands is too many and wanna sell. If no buy wall at all, they will find fooled by B&C. No one can predict what trade volume he will do in future, could he? This will increase their trading cost.

**When there is need, there is market.**There will be a BKC market with both sell wall and buy wall. At least, I can provide BKC manually: build buy wall at 0.9 NBT per BKC and sell slightly lower than official price. I only need to check my orders every week even month, Sounds a good business. LOL

It’s explicitly stated in the design document that no peg will be maintained. People don’t get angry at the US Postal Service when they buy too many postage stamps (usually!), and they shouldn’t be angry at B&C Exchange if they buy more BlockCredits than they need.

This will be no different than someone offering to purchase postage stamps with the hopes of selling underneath the US Postal Service. Opportunities for arbitrage in periods of temporary supply surpluses may actually create opportunities for profit. It’s likely you will be competing with many others who are willing to offer the same service however.

B&C DAC will spend Zero on BKC pegging and any BKC sale is gross profit.

I am just curious about the spontaneous BKC market, perhaps the coproduct is another relative stable currency: BKC. Very funny! If no one provide BKC buywall, I’ll do it without any authority’s permission, free market!

It will be comparatively stable with reference to something like btc. However, I expect the BKC buy walls to be placed down around $0.98 at best, possibly vastly lower, reflecting the sparseness of most alt-coin bid volume. Compared to liquidity operations this pegging mechanism is mostly just a suggestion of real-world worth. I think that once people are trading PPC for BKC for NBT for BKC for BTC for BKC for PPC, at the end of the day BKC will have a much more ephemeral connection to USD than NBT which is pegged using external price feeds.

(again, I’m super unsure I completely understand B&C. You have to go through BKC for every transaction right?)

This sort of BKC peg is certainly good in theory, but liquidity is a problem. If BKC is ever to be used outside the B&C exchange with large markets there will be serious liquidity issues.

BitUSD also maintains its peg by a theory of market competition and so far the lack of liquidity is not doing them justice. Not that we’re very clearly better at this point, for other shortcomings that we are hoping to patch. There is also an element of market expectations on the value of making a trade on B&C; if the B&C exchange fee is deemed too high perhaps the market will drive the BKC price downwards.

If BKC has a relatively stable peg, B&C not only gives NBT a better risk-free exchange, but also offers BKC as another agent for people to recognize the peg and a good source of buy-side liquidity. I’ve always been thinking what a partnership with BitUSD could do to NBT, but now BKC seems to be a good substitute. It’s a good thing.

I guess the economy of BKC might be like this - some people bought too many BKC and want to liquidate them so they put them up for sale at,e.g. $0.8. This could happen after initial euphoria cools off after B&C starts, as usually happens when a new technology comes out. Traders buy them and form a market to sell with profit.

I am wondering if B&C blockchain could automatically prune all exchange transactions and BKC tx after a year to curb blockchain size. If this is implemented block time (i.e. trade transaction delay) could be reduced by a lot. BKS tx will be preserved. The implication would also be that all B&C trades and bids/offers are forgotten after a year (funds of unfilled order will have been returned to sender using time-locked mechanism), and that all BKS has a limited shelf life of a year. This demurage will cause people to sell surplus BKS and provide a driver to secondary market.

Just a small point of clarification - transaction fees will be shareholder-configurable. It’s far more likely that the amount of BKC required to execute a trade will adjust if the market demands it, rather than the market demanding a new BKC sale price. There is no “peg” with BlockCredits, only a sale price.

Technically there is no peg that is held as a promise by the exchange, but if we only sell BKC at 1 USD then shareholders only see revenue when people are willing to buy BKC at or above 1 USD. On the other hand, shareholders will feel a bit ripped-off if the desired price of BKC is much higher than 1 USD. So the sweet spot is 1 USD or a little bit above 1 USD. Any mechanism that enforces this is desirable, so to me that is good grounds to talk about a “peg”, even if it has to be kept in quotes.

The future depends on what market capitalization of B&C and Nu are.

If B&C Cap. is above billions USD and much bigger than Nu’s, I bet people prefer BKC rather than NBT because BKC is issue by a big/profitable company and incentive of provide BKC buy wall is strong since it’s profitable.

Finally free market is the ultimate judge, and firstly loose peg supporter from Nu community will join BKC.

What’s your spread? I would suggest you increase beyond the 0.2% default. Or, you could try our fiat pools on bter or ccedk, or use NuLagoon’s ‘c’ pool which is not trustless but is not exposed to volatility losses.

I’m working on setting up CCEDK. I’m running on BTER. Of course any market that has less volume will be better for this. But ultimately I think NBT wants to see volume on all markets…so it is a catch.

Excuse me for being completely new, but how do you adjust the spread - in the conf file?

My experience after ~20 days.

I have been steadily increasing my contribution to the pools throughout. Also, I have been compounding the interest NBT received. I am equally spread throughout all of the pools, but I have less in the CNY/NBT pair because of the interest.

20 days = 4.88% profit

vs my projected profit of 5.34% based upon my distribution.