#Work in Progress

–Begin–

##Spread Band Model

In a single instance of a custodian, there are normally 3 prices that matter: the price feed, the bid price, and the ask price. Usually, the offset of the bid and ask from the price feed is symmetric and so the individual spread can simply be defined as (the ask price minus the price feed) divided by the price feed.

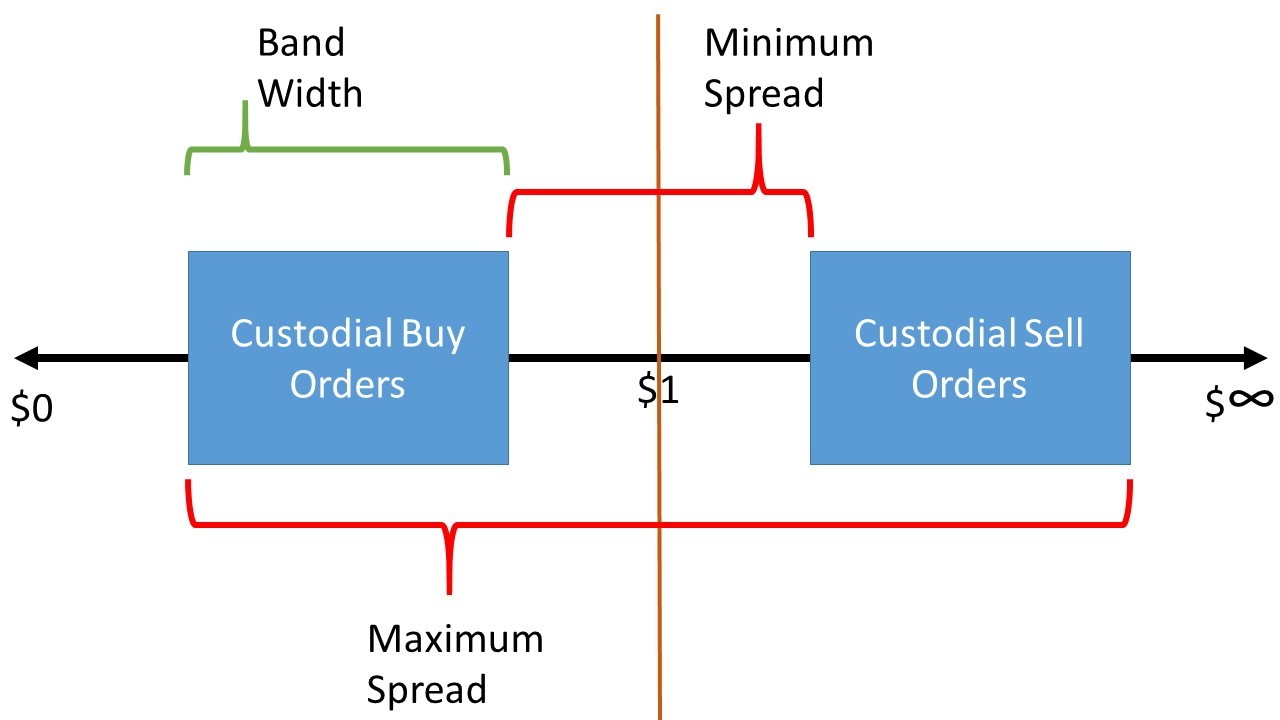

When several custodians provide on a single pair, there are potentially many bid, ask, and price feeds. The end result is that spread is no longer defined succinctly with a simple equation. Instead, there is some width to the bid and ask orders that we will call the spread band. The spread band can be defined using 3 parameters: maximum spread, minimum spread, and virtual price feed. As this is a stochastic effect, actual distributions of orders within the spread band will be beyond the scope of this motion. The virtual price feed will be described as the average between the two most separated orders in an operation.

The maximum spread minus the minimum spread gives the band width, a number that represents both the stochastic deviations of orders about a single price feed and the deviation amongst different price feeds. While it is understandable that operators may want to specify an individual spread when going through the grant proposal process, if they are to be compared with another operation that has a spread band it is the maximum spreads that should be compared. For example, twice the tolerance for an ALP is a maximum spread while an MLP operating NuBot has an individual spread equal to two times (the offset plus the fee). A participant in the ALP must set their individual spread to be strictly less (often by a non-trivial amount) than twice the tolerance if they wish to be paid consistently. To go from individual spread to maxmimum spread in the spread band model requires attention be paid to factors including potential deviations from a common price feed (orders can only be moved discretely and periodically, high frequency trading is beyond the scope of this motion) and deviations amongst different operators’ price feeds.

###What Spread Band Means for NuBot

A minimum band width should be approximated. While potentially empirical and ultimately beyond the scope of this motion, a good starting value would be the amount the price can deviate before an order moves. In NuBot this is the ‘WallShiftThreshold’. Further organization amongst liquidity providers (such as the price streamer) may even lead to a collapse of bandwidth to zero. In this case, the individual spread amongst different buy and sell orders can be anywhere between the regulated minimum and maximums. Otherwise, the regulations in this motion will apply to the operation’s proposed maximum and minimum spreads:

Minimum spread = individual spread - bandwidth

Maximum spread = individual spread + bandwidth

Nu Ownership

When an operation is created, it must be clarified whether it intends to be NuPaid or NuOwned. In most cases, this distinction will be quite obvious.

NuPaid - Nu provides periodic compensation for the operation. The operators are required to provide a report on the operation, either in the form of a direct custodial grant or as a prerequisite to receiving funding from T4 reserves. While it is preferable to end an operation on good terms with the provider, shareholders do have the power to withhold funding if the contents of a report are not to their liking. Most often, actual profit and loss is not accounted for due to the potential for anonymity in this arena, however that profit and loss should be incurred by the operation rather than Nu itself.

Current examples of NuPaid operations include NuPool and ALPs, NuLagoon, devs (when they don’t hold their own reserve)

NuOwned - Nu provides funds, either from T4 or direct custodial grant or some other mechanism, that become integrated in the operation. Shutting down an operation of this nature is more involved than a NuPaid operation because of the implication that the funds will be returned to the network in a transparent way. It is this implication that defines an operation as NuOwned and most NuOwned operations should either require collateral or require multiple signatures with shareholder elected custodians. NuOwned operations must present a periodic record of product and expenditures with a maximum period of 3 months (referred to as a quarter, counted from January 1st 2016 and beginning the quarter after the one in which this motion passes).

Current examples of NuOwned operations include gateways and executors, FLOT, T3 trusted trade, devs (when they hold their own reserves), JordanLee’s T4 single sig, NuSafe

Shareholders and Liquidity Providers Stand United

Minimum Spread = 0% SAF

Spread-after-fees, or SAF, is equal to the spread minus twice the exchange fee (once for ask and once for bid)

An operation with a minimum or negative spread can create order collisions unless the decision making is more centralized (like T4). Furthermore, when multiple operations exist on a similar exchange their collective band width may cause collision or extremely small spread. Profitable liquidity providing is beneficial for the network and shareholders will not motivate an operation that has a dangerously low minimum spread. Shareholders will require any T1 or 2 operation have a minimum spread of twice the exchange fee and no less than 0.01%.

###What 0% SAF Means for NuBot

As the fees are already taken into account, this simply states that the minimum bookoffset that should be encouraged is equal to the bandwidth, or 0% if price streamers are used.

Showing Deep Pockets and Providing Quality Liquidity

T1.1, T1.2 and T2

Distinction amongst the lower tiers is left as a question of maximum spread. Tier 1 is further broken down into high quality T1.1 liquidity and low quality T1.2 liquidity. All other liquidity on exchange is referred to as T2 liquidity, whether it is on the books at very high spread or simply sitting on-exchange.

To give a show of deep high quality liquidity, all NuPaid operations that propose to act on T1 must act as T1.1 liquidity. On the other hand, NuOwned operations may act as T1.2 liquidity with a portion of their T1 funds. This distinction is made because of the tendency of NuOwned operations to be of greatly reduced continuous cost whereas NuPaid operations often compose a large operational budget. The philosophy is that if we are paying top dollar we want the highest quality of liquidity.

This new regulation cannot be interpreted as modifying any existing contract for liquidity provision. It merely mandates that all new proposals comply within the maximum spreads defined. This means existing liquidity pools will become compliant when their next contract passes.

There is an exemption for trading pairs with illiquid assets. Liquid assets shall be defined as Bitcoin, Ether, Litecoin and stable government currencies such as USD, EUR and CNY. All other assets are considered illiquid and any pool may operate in T1.2 freely.

Paying for a Tight Peg

Maximum T1.1 Spread = 1%

No NuPaid operation will have a maximum spread of greater than 1%, which will be defined as T1.1. Therefore, Nu will not pay direct compensation for a pair of orders that have more than 1% separation (normalized using a virtual price feed as described in the spread band model). Any operation that cannot provide a method of keeping orders between the minimum and maximum spreads as defined by this motion will no longer be acceptable to shareholders.

###What a Tight Peg Means for NuBot

If bandwidth is 0%, this requirement simply states that NuBots should be using a bookoffset between 0% and (0.5% - fee) while ALP v2 set a tolerance of 0.5%. If bandwidth is x%, bookoffset should be between (0+x)% and (0.5% - x% - fee). Parametric orderbook can be used, but only if care is paid to stay below the maximum spread.

Direct Involvement in Market Supply

Maximum T1.2 Spread = 5%

NuOwned operations define T1.2 funds as those within 5% spread and may report T1 liquidity as such. If NuOwned operations act on T1.2 they must keep a minimum of 1000 NBT on T1.1. Additional funds may be placed at any spread greater than 5% but must be reported as T2. It is expected that these operations will portray a deep liquidity connection to T4 at potentially wider spread so as to promote free market and NuPaid operations to seek profit by tightening their spread.

What Direct Involvement Means for NuBot

Parametric order book is fine, but only for T1. T2 cannot be placed yet with current software. For T1, make sure the first order is on T1.1 and at least 1000 NBT, then make sure the rest of the walls have an offset lower than (2.5% - bandwidth - fee). A good rule of thumb would be to keep it under 2%. As an example:

“bookSellwall”: 2000.0,

“bookSellOffset”: 0.003,

“bookSellInterval”: 0.004,

“bookSellMaxVolumeCumulative” : 10000.0,

P&L for Nu Owned Operations

For each counterparty currency and NuBit pair, calculate the following:

Product = (Average price of NuBits sold)(Volume sold)

Expenditure = (Average price of NuBits bought)(Volume bought)

Flux = (Volume Sold) - (Volume Bought)

P&L = [(Average price of NuBits sold) - (average price of NuBits bought)] * min (volume bought , volume sold)

Injecting Funds in a Crisis

Minimum T4 spread = -5%

During an extreme event, T4 may need to move money very quickly and may offer a premium to traders willing to do that. However, NuOwned T4 operations may not have a spread of less than -5%. This direct market incentive is considered more than plenty to stimulate market activity and any further reduction of sell price or increase of buy price is to be considered inappropriate for a NuOwned operation. If current operations are still failing the peg by T4 standards there is most likely a more systemic issue that must be addressed.

–End–