If there’s so little funds at exchanges, please remind me: what is NuLagoon getting compensated for?

For mainly T3?

Or for NuLagoon Tube, with that NuLagoon earns fees (except when trading with FLOT)?

If there’s so little funds at exchanges, please remind me: what is NuLagoon getting compensated for?

For mainly T3?

Or for NuLagoon Tube, with that NuLagoon earns fees (except when trading with FLOT)?

Keeping the Nubits pegging at $1 is our top1 piority. If the peg is in dangrous, we will not hesitate to provide as much liquidity as we could. Addtionly, there are motions regulating how NuLagoon provide liquidity support on behalf of Nu Shareholders. We will act accordingly.

Thank you very much for your service, but I need to say that there have been more occassions than I can count, at which the peg was solely kept by NuBots (and very recently a PyBot as well) that operated with Nu funds.

But I think the discussion fits better here:

I was originally focussing on ALP when I started that thread.

Maybe the view needs to be widened.

@henry: keep NuBot at Poloniex running and funded.

By design your MLP operation there should serve trading customers before the Nu funded NuBots/PyBot need to kick in.

Hi all,

I’m a NSR holder and first-time poster here . I’ve been watching the NuBits project since it’s beginnings on the Peercoin forum.

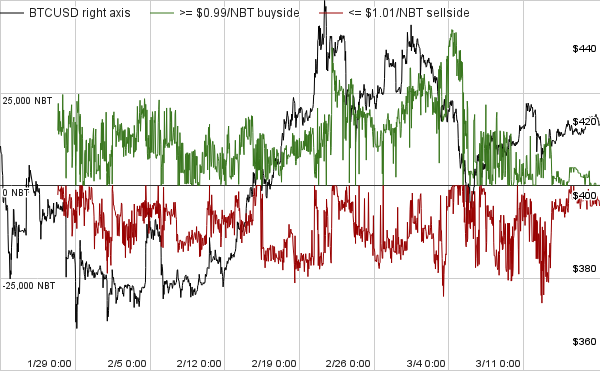

I’ve developed a real-time chart in Google Sheets that I use to monitor how well the peg is kept to $1.00 USD on the BTC/NBT pair on Poloniex. I figure it is relevant to this thread and would maybe help efforts in keeping track of the peg. It shows buyside liquidity that is at-or-above $0.99/NBT and sellside liquidity that is at-or-below $1.01/NBT. The price of BTC is also graphed, and is based on Bitfinex’s BTCUSD rate. Data are updated at least once per hour, and more frequently when the BTCUSD rate is changing rapidly.

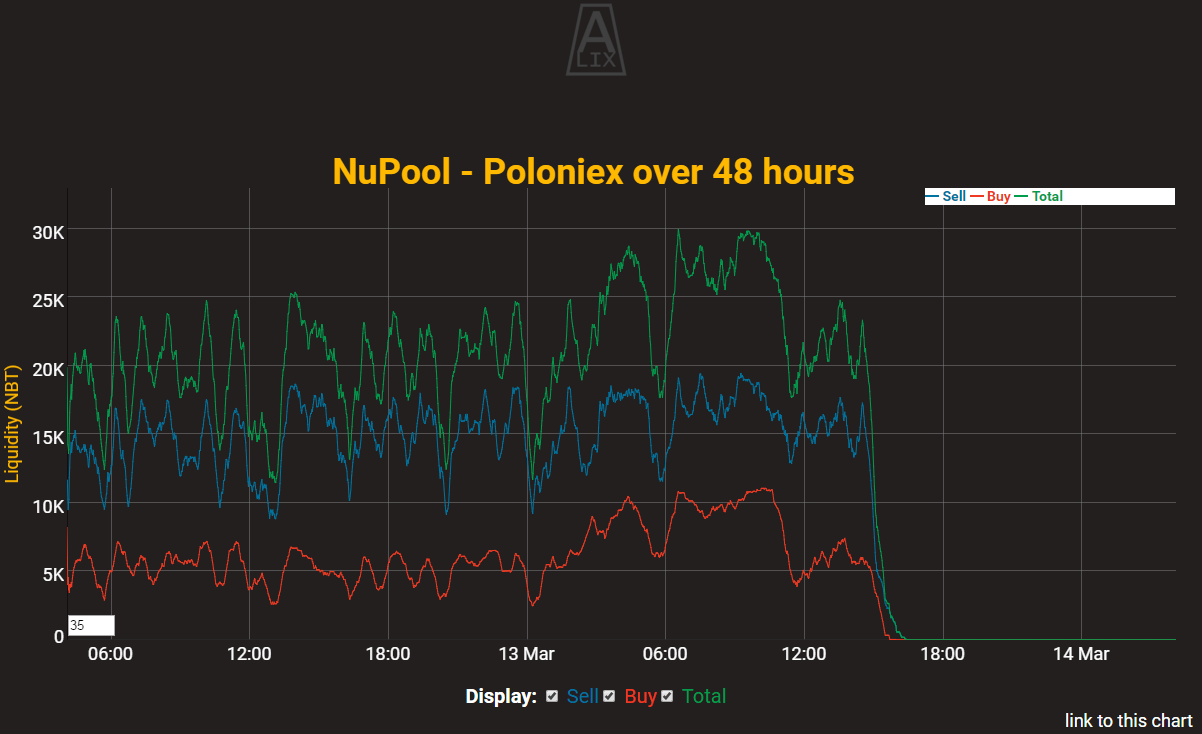

I started tracking data at the end of January. Liquidity has declined dramatically since 3/13/16.

Click here to see the real-time chart

Here is the chart current as of this post:

Can someone more familiar with liquidity operations explain why this has occurred?

What is the best way to ensure we have $20,000 or more on each side at Poloniex 90% of the time?

Nu-pool operations have stopped recently and abruptly as they ran out of funds before a new grant was obtained. Liquidity operations are now running on NuBots and a Pybot funded by FLOT.

There also appears to be some intermittent issues with NuLagoon’s NuBot on Poloniex, this requires further clarification and is being monitored by some in the community.

Short term, FLOT can increase the funds held on exchange increasing the risk profile of NuShareholders’ funds.

Passing of the grant for Nu-Pool on ALPv2 will probably provide some relief and hopefully more stable provisioning of liquidity due to the new reward model.

Clarification from NuLagoon is required about the apparently lower service levels recently.

Nubots have more than 20000$ in T1+T2 in Poloniex currently. But they provide merely 6000$

at the 1-2% spread. Even if ALP was operational, we can’t know how users would behave

Thus we need more nubot gateways + increase the T1 supply.

Following my invoking of the need for a paradigm shift, allow me to start answering your question by asking an additional one:

what shall be the offset or spread for those $20,000?

Speaking of Poloniex and ALPv2, I envision a maximum of few thousand USD ($2,000 - $3,000) each side at a quite small spread (<1%) provided by ALP.

The rest of the liquidity on the order book will provided by Nu funded NuBots, which operate at above 1% (e.g. at an offset of 1% and with parametric order book in parts way above 1%).

This way

Under normal circumstances the combination of ALP and Nu funded bots is reducing the efforts for liquidity provision on Nu side (ALP have an incentive to keep funds there and balance sides), keeping the spread quite tight for small trading volumes and having sufficient liquidity for trading whales who don’t care about some percent offset when trying to bet against Nu.

But most importantly: this way Nu doesn’t have to rely on ALP to provide liquidity at any exchange; liquidity can be provided by Nu - following and evolving the “gateway idea” I spawned last year.

Give NuLagoon’s money to nupool ALP v2. Use 40k target with $5,000/month CRFC for a total of 0.4% average rates when operating under target. Keep spread and everything else the same. If the pool has a 3:1 sell:buy ratio under target (for example 10k buy and 30k sell) this will cause rates to spike to 0.8% on the buy side.

Next, people will be begging for T3 custodial contracts so they can get to the deficient side with low friction.

It is important to set high rates when the pool is under target. If you scoff at the $5k, the reaction should be to decrease total cost and target in proportion, not to drop the 0.4%. Not that 0.4% is a magic number, but it should not be as low as the fixed reward pools of 0.2% or it wont work as well. The difference in philosophy is that fixed reward targets are maximums while CRFC targets are minimums.

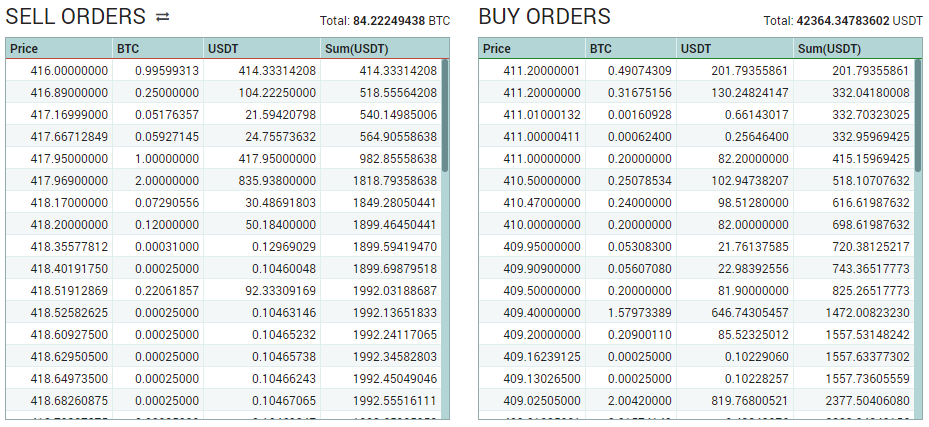

Regarding $20k each side - if you look at the liquidity of one of our competitors (Tether) at Poloniex, you see that the spread for the last orders is over 2% (418/409=1.022) if you want to trade more than $2,000 volume:

With a

Nu would offer the better experience compared to Tether

It would be great to have the pair flipped from NBT/BTC to BTC/NBT to have “USD” values for the NBT orders instead of 1/USD…

For reference: the order book of NBT

Without ALP Nu offers more or less the same spread, but with much more volume at a quite small spread (~ 4,000 NBT on sell side at or below 0.00242219; over 4,000 NBT on buy side at or below 0.00236446; 2.4% spread).

If we’re going to bother Poloniex with switching the pair, then we should tell them to switch the name while they’re at it. Have them change it to BTC/US-NBT.

Also, is it me or is there an entire section dedicated to Tether pairs on Poloniex? Why were we not able to convince them into doing the same for us? Did we even make an attempt?

I’m of the opinion that most of Polo’s verification system has to do with kyc/aml requirements imposed by tether. I don’t really know, but that’s my opinion. Of course if they’re going to all that effort then they want to make it a big feature on their exchange that they accept tether.

That’s a plausible assumption.

…and even with the currently degraded liquidity provision at Poloniex, Nu offers the better trading experience

Except we dont have an eth/nbt pair. Eth/usdt is 131k volume today. Basically it accounts for all the btc/usdt volume every day.

I know of at least one person who said they went with Tether over NuBits because they offer bank withdrawals, although they didn’t like the experience…

###Gateway status at Poloniex

Fri Mar 18 19:32:03 UTC 2016

status of mOD dual side NuBot at Poloniex:

nud getliquidityinfo B | grep BFGMPykfKxXZ1otrCZcsbnTwJjKHPP9dsP -A 2

"BFGMPykfKxXZ1otrCZcsbnTwJjKHPP9dsP" : {

"buy" : 23735.9045,

"sell" : 6251.84

status of zoro dual side NuBot at Poloniex:

nud getliquidityinfo B | grep BJs4YbtaqCmxeHLiR6zzjnZEotYVFAPfMo -A 2

"BJs4YbtaqCmxeHLiR6zzjnZEotYVFAPfMo" : {

"buy" : 8867.4665,

"sell" : 17053.8345

status of Cybnate dual side PyBot at Poloniex:

nud getliquiditydetails B | grep B954pkUEdkeT1G5Lq14Cisij5no3RVxHYe -A 20 | grep poloniex -A 2

"1:NBTBTC:poloniex:LiquidBits" : {

"buy" : 0.0,

"sell" : 1600.0

status of NuLagoon dual side NuBot at Poloniex:

nud getliquiditydetails B | grep BTRnV9uLSPVJw4jn1JMV2Ki2cfFqPYip9o -A 100 | grep poloniex -A 2 | tail -n 3

"1:NBTBTC:poloniex:0.3.2a_1457865931788_81cb7a" : {

"buy" : 0.0,

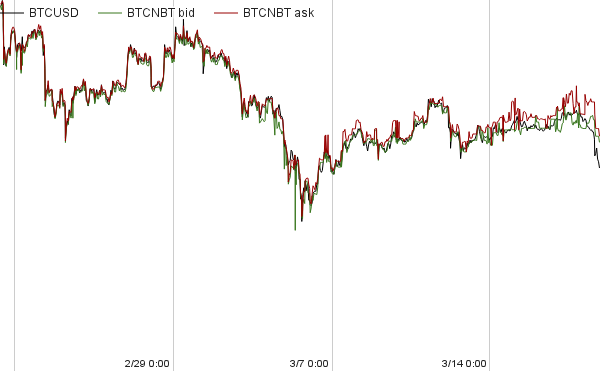

"sell" : 1951.8654Also, the BTCNBT peg Poloniex is drifting and not closely following BTCUSD(Bitfinex):

At the moment there’s no ALP at Poloniex due to NuPool rebuilding the ALP server on NuBot (ALPv2) instead of PyBot.

It’s NuBots and one PyBot who provide liquidity at Poloniex at the moment.

The NuBots (except the one from NuLagoon) and the PyBot have a bigger offset or spread than the ALP.

Speaking of NuLagoon:

@henry, is something wrong with NuLagoon’s NuBot at Poloniex?

Session ID 0.3.2a_1457865931788_81cb7a seems to be the current one, but there’s nothing on T1:

nud getliquiditydetails B | grep BTRnV9uLSPVJw4jn1JMV2Ki2cfFqPYip9o -A 1000 | grep 0.3.2a_1457865931788_81cb7a -A 2

"1:NBTBTC:poloniex:0.3.2a_1457865931788_81cb7a" : {

"buy" : 0.0,

"sell" : 0.0

--

"2:NBTBTC:poloniex:0.3.2a_1457865931788_81cb7a" : {

"buy" : 3517.6,

"sell" : 701.1925The session is already some days old. Maybe NuBot needs to be kicked?

To catch this arbitrage opportunit one has to use the NBT/USD pair which is only available on CCEDK. Direct NBT-USD exchange could help.