When we talk about BKC and NBT, both appear to be equal to $1 and a 1:1 peg seems natural. However, as B&C sells BKC for $1 but does not buy them back, BKC is always <$1, whereas NBT is always ~$1. That means that they may have very different real values. It quickly becomes clear that B&C is destined to profit from a 1:1 peg at the cost of Nu.

So what if Nu lets that happen, but charges B&C to do it? More specifically, what if Nu liquidity providers are awarded BKS for using their NBT to support a weak BKC peg? It could be a tiered kind of thing, such that a buy order that is close to 1 BKC = 1 NBT is awarded more than an order at 1 BKC = 0.5 NBT. By only paying the buy side liquidity and doing it all internal to the B&C exchange, the reward necessary to stimulate a healthy buy side may end up being very cheap.

This does not affect Nu very much (no motion necessary) except that it gives additional business and possibly even healthy competition for liquidity providers (drawing them from pairs like nbt/btc and into nbt/bkc). B&C would need to be printing the BKS, so the question is whether BKC buy liquidity is worth it to them (at something like 0.5 NBT/BKC I think it would be worth it).

Is this method cheaper than selling BKS to buy back BKC?

I think we’ll find that if the BKS market is illiquid the answer is yes.

I’m a little leary on printing BKS to do this because I’m not sure how much dilution it will take. Couldn’t we just convert some of the profit from BlockCredit sales to NuBits and use that instead? No dilution necessary right?

Or B&C could just pay NuShareholders to keep it at $1 and have us do all the liquidity work.

Why would we want to buyback BKC? I see no reason for doing this, if people buy more BKC then they use they’ll end up selling these amongst themselves. No reason for us to maintain a peg.

I don’t understand the logic? The value of BKC will float between $1.00 and whatever the secondary market (like @Sabreiib) offers to buy unused BKC at. I could see buy-side support settling somewhere around $0.95. Because BKC aren’t intended for general trade, they don’t really have value outside of the B&C Exchange ecosystem.

Why would a BKC peg be supported? BlockShareholders couldn’t care less what happens once a BKC is sold and a Bitcoin dividend is returned to them. A BlockCredit sale is obligation-free revenue in their pocket as long as the B&C Exchange trading platform is operational. The absence of responsibility to secure a long-term stable value for BKC is a benefit for BlockShareholders.

If B&C is doing well then for whatever reason does less well, there will be a lot of BKC on the market. In that case there is a third person in this situation, the person who is selling BKC for less than $1. At that point, B&C is selling BKC at a premium to only people who want the convenience of not having to buy it on the open market.

If there are so many BKC on the market that the price of 1 BKC is $0.5, what is the best option for B&C? Clearly, they won’t be distributing dividends for a while. What happens if they want a little extra money for developers? The only option is to print BKS. Isn’t it better to give that BKS to Nu liquidity providers than to sell it on the open market or to give it to the developers who will sell it on the open market? (If the developer accepts BKS we should just pay them in that, this is the case when the developer needs to pay their bills).

If there is so much BKC on the market then we’ve already made a ton of revenue, while we’re making revenue we need to plan ahead on what additional funds we might need for development and set aside some of our revenue for this. That in my opinion is always the better option than diluting shares, something which I’m heavily against. Maintaining a peg costs money, the only way it would make us money is by buying lots of cheap BKC and then selling them back at a higher price later. I do not see a market for this developing however. I think we’ll see some BKC being traded due to people overbuying but it’s my expectation that this will be small amounts not worth a peg. There might be some smart individuals buying up BKC for 90 cents and selling them for 95 cents but I don’t see this becoming a big market.

Initially, I will provide BTC/BKC liquidity on 0.9$ buy and 0.99$ sell.

I won’t use NBT pair because I guess many B&C customers prefer to hold BTC rather than NBT.

2)My initial liquidity is around 2000$, it’s small, I cannot predict the sizeof the BKC secondary market.

All I need is a BKCbot which can be slightly modified version of Nubot. I don’t have to get BKS holders’ permission, I am a free man for my own business. My trade section may be [0.9,0.99] or [0.5,0.8] whatever I think, risk and get profit on my own. Pegging with spread is the perfect fit for antiinflation pegging and certainly I hope BKC liquidity increase as much as possible after more and more joining me.

Everything you’ve said is exactly why I think it’ll be cheaper for BKS holders to pay Nu to provide the liquidity software than for them to perform a BKC buyback.

And yes, pegging with large spread is essentially what I’m talking about, but only buy side.

Why do you think so? The design document clearly suggests that BKC buybacks should never happen. BlockShareholders have zero obligations to a user who holds BKC as far as redemption value is concerned.

While BlockCredits are the same as NuBits to the code base, they have a completely different purpose. They are solely for use as transaction fees and are not intended for general trade as NuBits are. Accordingly, a peg for BlockCredits will not be maintained. They are comparable to postage stamps in many ways. They are sold with the promise you will receive one US dollar worth of transactions on the B&C Exchange. Just as you wouldn’t expect to be able to sell postage stamps to a third party at face value, there shouldn’t be an expectation that BlockCredits can be sold for one US dollar, although a resale market may appear. BlockCredits should only be purchased with the intent of consuming them to pay transaction fees on the B&C Exchange.

The United States Postal Service does not offer to buy back postage stamps once they are sold because they are considered good and valid. BlockCredits should be no different to B&C Exchange.

I’m proposing an alternative to buybacks if B&C goes deep into the red. The US doesn’t buy back stamps because a) it’s illegal to sell stamps on the street and b) people still buy stamps from the US postal service.

I guess I’m a little early to be thinking about the entire economic cycle of B&C. Maybe it’ll all be roses and sunshine for the entire lifetime of B&C.

Nu has the ear of the liquidity providers, has experienced pool operators, tech support, trading bot development, you name it. Liquidity is Nu’s game. Why would B&C try to do Nu’s job while also doing its own?

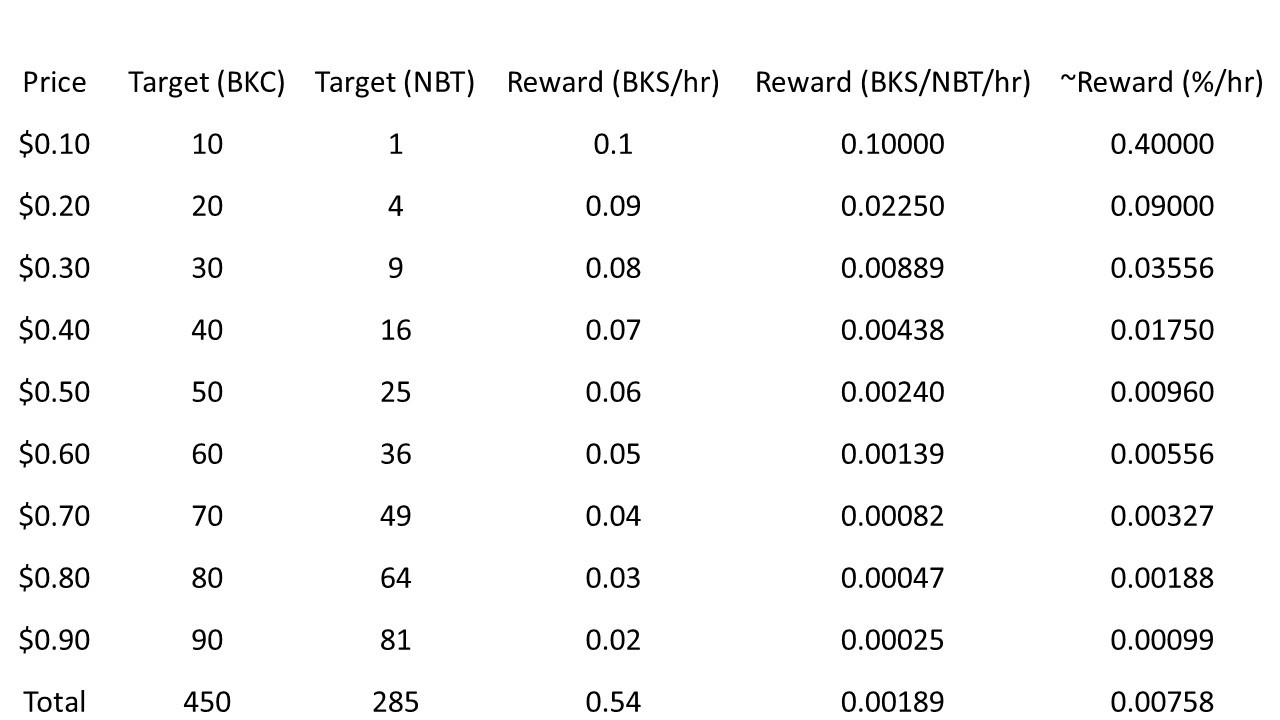

So here’s the technical conundrum of the BKC/NBT peg:

We want to stimulate people to place their orders as high as possible. However, we want to award people more when their orders are forced to be low because that means that they are doing more to help B&C. So you want to award them for placing buy orders just below the sell pressure.

The only solution I can think of is the good ol’ price-volume solution. Have slots at different prices with different target volumes that give different rewards. The slots are filled from lowest to highest by the server (not as trustless as TLLP because the price feed is essentially coming from the operator) and rewards are given out at the end of some period (call it 1 hour). At the end of the period, all liquidity is randomly reshuffled such that everyone has an even chance at the highest paying, lowest risk slots. The server would keep ordermatch=true at all times.

A set up like that would cost less than $200/year at a price of $4/bks. The approximate reward % column assumes a price of $4/bks.

Maybe this isn’t economically viable, I don’t know, I’m making it up as I go. In my mind, this is a way of spending BKS to turn around a sharp BKC depression that’s more efficient than a BKC buyback. The parameters could be adjusted somehow (shareholder voting?) such that B&C spends more shares when the price is low. Perhaps the ‘Reward (BKS/hr)’ column should be multiplied by (1-x) where x is the achieved fraction of liquidity target.

As a BKS holder, I refuse to dilute BKS and refuse to expend money on BKC liquidity, if B&C business cannot provide enough profit by charging transaction fee to cover software devepolent and other expenditure, I’ll quit.

So you aren’t going to vote on any more BKS dilution grants? How do we fund development before we start making Txn fees?

The point I’m trying to make is that the BKS dilution will happen on the down side of the economic cycle. If we drag our heels and say “no”, B&C will stop distributing dividends and the market cap will drop. Eventually, when the shareholders that refuse to dilute ‘quit’, they will be replaced by shareholders who will take action during an economic downturn. Shareholder evolution.

Anyway, I’m too early for this. I’ll come back to this topic when BKC is being sold for <$0.8

So you aren’t going to vote on any more BKS dilution grants? How do we fund development before we start making Txn fees?

If we reley on share dilution on a regular basis, the DAC is failed.

If exchange income does not cover expenditure, it should be closed, bankrupted. The basic trading function will be available after months. Our revenue maybe small initially, but our expenditure is even smaller. At least NBT LPCs will pay some BKC, How much money cost to run B&C DAC’s network? My computer power consumption? Internet service fee? neglectable at all. We don’t need to pay LPC rewards as Nu has to do. If there are BKC LPCs in future, they are also seld-funded and self paid. Never give them a single penny.

I am not completely opposite to share dilution, it can be done in VERY VERY rare cases, of course other BKS holders perhaps don’t share same opinion as mine, but that’s my two cents.

And that revenue can very well be split in a part that gets paid out as dividend and a part that gets sent to an NBT multi signature custodial address of a “development fund”.

Say the BKS holders would like to fund project X that is not time-critical. They could create a motion to send a percentage of BKC sale to the corresponding development fund. Once the funding is far enough, development can begin.

All without BKS dilution!

…in a perfect market the difference between distributing all revenue as dividends and issue BKS to fund development and the solution outlined above would be 0. But we aren’t operating in a perfect market.

Furturemore, there will be reputed signers election campaign. Some candidate may say to community"Hey, I will donate 1000$ of BKC/BTC to that development fund, my donation is recorded on blockchain so that everyone can check it, since I’ve shown my honest with my real money, please vote for me!"

In next version, B&C wallet may add a data that shows how many BTC/BKC a reputed siger has donated to community.

How much money cost to run B&C DAC’s network? My computer power consumption? Internet service fee? neglectable at all. We don’t need to pay LPC rewards as Nu has to do. If there are BKC LPCs in future, they are also seld-funded and self paid. Never give them a single penny.

How much money cost to run B&C DAC’s network? My computer power consumption? Internet service fee? neglectable at all. We don’t need to pay LPC rewards as Nu has to do. If there are BKC LPCs in future, they are also seld-funded and self paid. Never give them a single penny.