Thanks. I think i made it.

Before, i used the site

http://hash.online-convert.com/ripemd160-generator

and i got a different result!

How much is expected to be deposited into this gateway and what if you run with the funds?

In other words, I think we should now impose a collateral from the gateway manager.

I expect such proposals to include a collateral from now on.

1 Like

Collateral would drastically raise the bar for this operation, because the operator would be forced to deal with the risk of exchange default instead of Nu. This operation is intended to be cheap and risky and make shareholders painfully aware of the gaps in the current liquidity model.

T3 can be collateralized because the custodian takes little to no risk and so the only thing they are collateralizing is the possibility that they may run with the funds or make an operator error, both of which are entirely within their control.

1 Like

Collateral is the same as MLP. This is a passive Nubot proposal. I have written about the risks. You decide

1 Like

Not exactly the same, but damn close.

That 0 NBT seems to be causing trouble.

I’ve added this combination into my personal data feed and my client keeps crashing every time it fetches the data feed.

So far I’ve been able to reproduce this behaviour with 2.1 RC 8 multiple times.

Changing the value to “1” or removing the address solves the constant crashes.

I already notified @coingame about this.

Meanwhile I would like to ask our data feed providers @cryptog, @cybnate and @crypto_coiner to NOT add this custodial address until this error is resolved.

The potential is quite huge if data feeds can crash half or more of our network!

4 Likes

Thanks for the info!

Then i should make it 1 NBT?

Yes, if you look through past voted in custodians the minimum value you can enter is 1. 0 will break things.

2 Likes

Can you elaborate?

As Nagalim corrects me, it is similar not exaclty the same.

It means that the LP risks his/her own funds in the exchange in case of collateral as in case of MLP or ALP.

adding this to my voting data feed – this grant proposal is a direct kaizen execution of MoD last proposal to support the peg besides MLP and ALP

ac2fd99c21e6021a3cecf3e7bc0d8f9d3b65439e verified.

I think we should impose a collateral or make the gateway manager bear the risk for the reward he or she earns in the near future but this proposal is a necessary band aid solution.

Voting.

There’s no reward from trading the funds, which the operator earns. All funds on a related account belong to Nu. All deposits and withdrawals come from or go to Nu addresses.

The operator receives a compensation for the efforts. That’s all.

You can require a collateral in the future. In the end this will either be more expensive for Nu (due to the compensation for the collateral) or skin the operator.

2 Likes

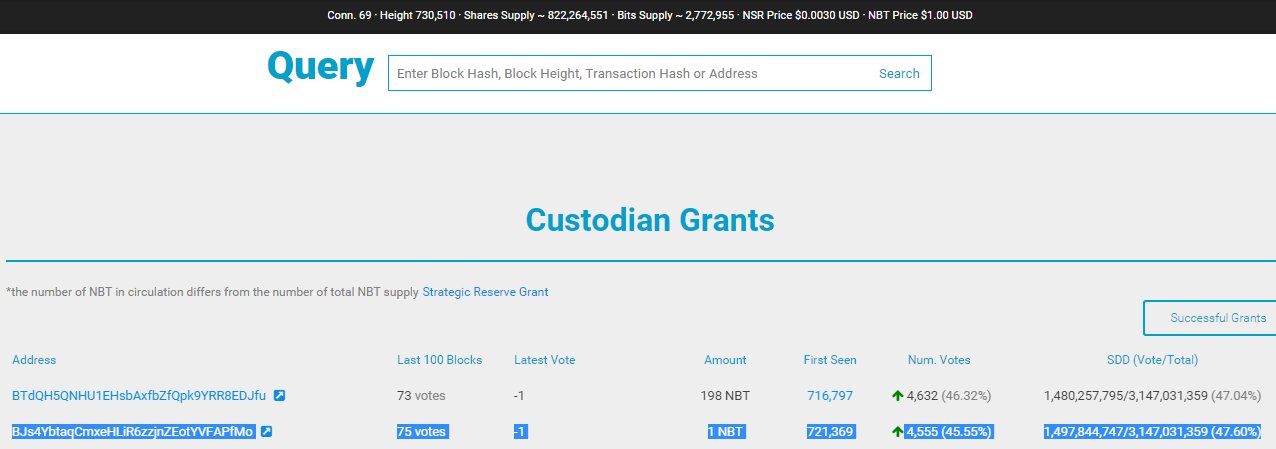

Your grant to retrieve a custodial address for broadcasting the liquidity is about to pass soon:

How far are your NuBot and Poloniex account preparations?

Poloniex is ready. I need only a credential file for nubot.

It passed. Thank you all!

When i get the credential file i will setup the nubot and make a new thread with accounting and other info about nubot.

2 Likes

It’s time to ramp up your operation.

I started emptying the accounts of the NuBots I operate to FLOT addresses.

After the reset of the withdrawal limit, I’m going to continue - the next withdrawal will leave the accounts empty and Nu with no second line of defence on Poloniex, if ALP is again unavailable during the next Bitcoin roller-coaster.

1 Like

well zoro’s nubot gateways should help right?

Right. Wouldn’t hurt to have backup for them. Don’t let zoro alone with that!

This is still a draft:

2 Likes