…and we would be liquidity wise in a bad situation, if all liquidity were at below 1% spread.

Just have a look at the recent events (BTC price jump), that drained all funds from buy side, that were at a tight spread.

Only the NuBot @zoro operates has a significant amount of BTC ($9,000) left.

This NuBot operates at a spread outside what ALix records.

Would you feel comfortable with this situation if there’d be no additional $9,000 BTC at an increased spread?

Hope you are not serious with your statement. If this motion, how much I don’t like it myself too, passes we will have to oblige. Of course you can choose to not extent your operation and transfer the funds back to FLOT. I might do the same.

Well, i was thinking about that. In fact it is FLOT that mandates my nubot’s settings. I am a single person, i cannot mandate NU’s strategy. Lets see how this will advance

Please note that the shareholder funding of gateways is different from other models since we do not reward the provision per se (there is only an operator management fee) and we use the Nu owned funds (NuOwned liquidity operation).

Besides, I suppose (please correct me if I wrong) that you assume that all shareholder funded liquidity is then broadcast in the QT client as either T1 T2 or T3 .

I believe that we want to have the best liquidity broadcast into the client with a spread lower or equal to 1%.

Perhaps we can make sure that liquidity offered at spread higher than 1% does not get broadcast but nonetheless can be found on the order books. In that case we could create another Tier. Right now, it seems that it is called T1.2 as defined here.

Right now, I believe the client does not broadcast T1.2 as it only considers liquidity whose spread is lower than 1%.

NuBot broadcasts the first order, that gets placed, as T1, all others at T2 - even if the offset is 5%.

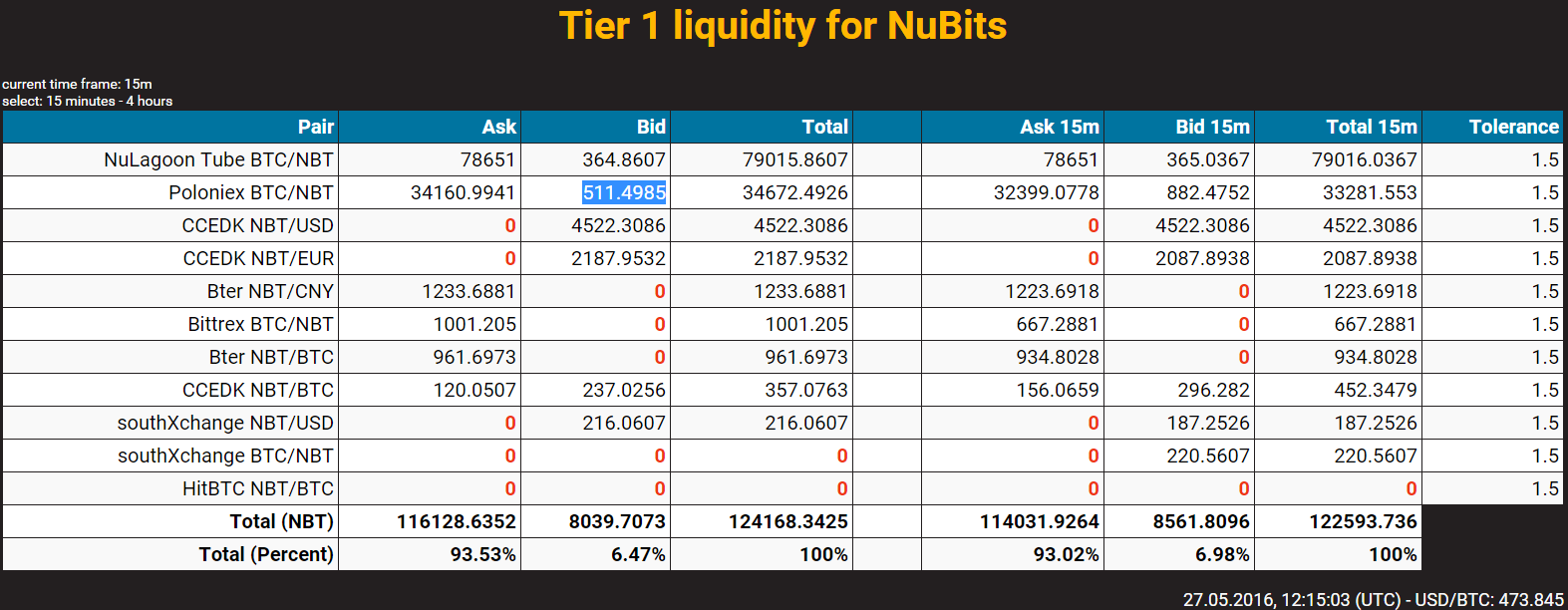

Have a look at getliquiditydetails of the current sessions of @zoro’s and my NuBot.

Tks for the pointer as always!

I see.

Technically it should not be called T2 though.

Anyway it does not change the idea.

I think broadcast liquidity should display only liquidity whose spread is lower than 1%.

We have different types of liquidity at different quality.

I don’t see a big issue here.

Supporting all trading pairs at all exchanges with high liquidity at a tight spread under all circumstances is wishful thinking, but not realiatically possible!

We should start differentiating between pegs in NBT/USD and crypto trading pairs (and when speaking of those differentiating with ones that have high liquidity and those that don’t), though.

In accordance with my support now for Jordan’s vision to re-try the original model of LP,

for lack of a better vision and alternative to restore the real peg, I am now supporting this motion.

Will add this to my data feed.

My understanding is that MoD’s version allows but doesn’'t mandates >1%, where FLOT can still instruct the gateways to <1%. It just leaves space to operate.

Ditto. I believe I’ve been convinced by Jordan’s arguments. I’ll go along with this and keep my fingers crossed that we can come out of this crisis in one piece.

Yes, buy wall @0.995 and @0.95 cost almost same money but send out different signal.

If Nu is lucky enough, more NBT will be sold, but not all customers will come back because of this crisis, I’m afraid NSR will suffer long time low price to pay Nu’s debts. This is a painful lesson, hope shareholders become smarter in future.

I have not been able to follow liquidity operations as much as you guys because of lack of time in the last year, so no, I unfortunately don’t know everything, especially all the acronyms. I feel as if his argument is correct though. It makes sense to me. I have limited knowledge on this though, so others please make up your own minds and don’t just follow me. I will keep reading replies to see what others think, but for now I’m voting for it. That could always change though.