As a data feed provider, I have not made my mind yet but I will make a decision today.

I think there are 2 things that we need to do from a business perpsective.

provide a lot of very good liquidity (tight spread <=1%)

have a way to limit our costs (bleeding) to protect ourselves (some liquidity at low quality spread )

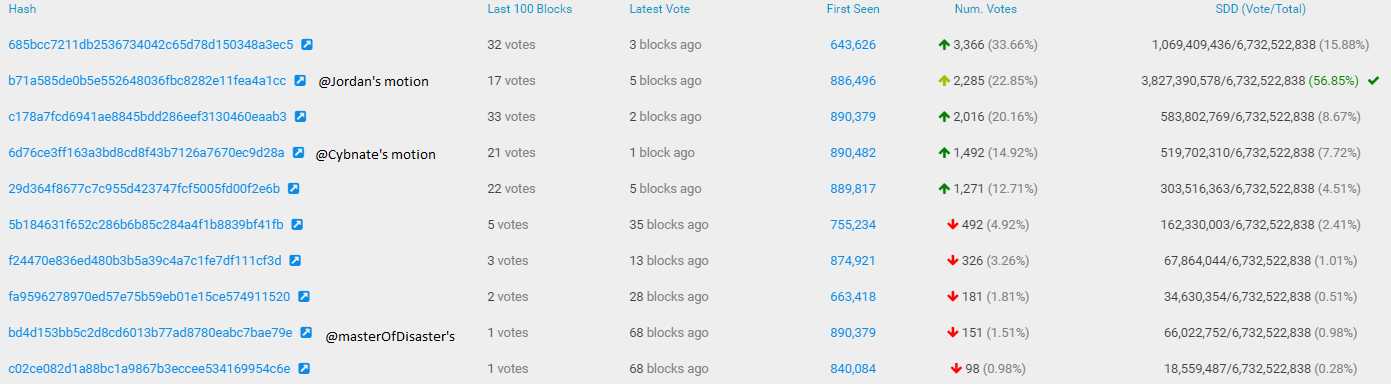

So in that sense, I think your motion or the motion made by @Nagalim or the motion made by @Cybnate are the most appropriate.

But there is one concern: there might be some chance that most of the liquidity is provided at a low quality spread.

We need to make sure that most of the liquidity is provided at a high quality peg.

This seems to be difficult to be specified in a motion.

My motion is the only one providing percentages of high (60%), medium(30%) and low quality (10%) peg, although I have to admit the percentages are a bit arbitrary but I believe a good starting point lacking fundamentals to work with. Mostly based on the actual situation except that the high quality is not there.

I’m curious - what makes those more appropriate than my version? I understand that for @Nagalim’s version, which is in the end a just a much much more precise version than I drafted.

Why do you find a maximum of 2.5% sufficient to defend the peg? @zoro’s NuBot runs close to that spread and already traded already one third of the funds in the last day.

Market awareness might require even bigger spreads than that…

Sorry for being unclear.

I did not mean that cybnate s version is more appropriate than yours just that it seems that the 3 other versions look more reasonable than jordan lee s version.

As explained here the percentage doesn’t need to be programmed in NuBot gateways. Even better if they are not. They just reflect the amounts the gateway holds on behalf of FLOT. This is based on contracts of e.g. 1-3 months and should be adjusted not more than once a month. It is not a percentage that should be changed every hour of the day.

It would be especially great to have an explanation from those who vote for one of the competing motions.

What am I doing wrong?

Why don’t you realize that all that keeps the peg on the current level is an offset far beyond what the competing motions allow?

What else do you need to make up your mind?

All that keeps the peg fixed above $0.95 is the gateways.

CMC speaks volumes.

$0.95 translates into an offset of up to 10% (I say “up to”, because in fact it’s not 10%, what I’ve configured in NuBot, because the sellside has a smaller offset).

This is only allowed by this very motion for exactly the reason we use the gateways at the moment: as a last line of defence.

Were @Cybnate’s or @JordanLee’s motion in place there’d be very likely no BTC left in buy side most of the time and NBT would likely have been below $0.95.

If you want evidence, zoro and me can configure a smaller buyside offset, but I’d rather not.

Why is it so hard to read and understand what I write?

Do I write to much and a “mOD filter” gets applied by readers?

I should stop caring, if only I could…

There is no doubt that gateways pioneered by you have been very useful once again (a second time), in fact crucial in protecting the peg by giving a financial disincentive (increase cost of exchange because of a high spread) to traders. Traders refrained from selling back their nubits at all or a large quantity of their holdings when facing a large spread.

But going forward do we really want to prevent traders from trading back their nubits?

I think the answer is no.

Nevertheless we need some protection.

Instead of a 5% spread above and below the perfect peg 1nbt=1usd, what if we used larger spread like 10% or 20%?

It would further increase the protection of the peg while at the same time prevent the use of Nubits.

So in essence I think large spread prevent users to use nubits.

This is not what we want ultimately.

This is why i think large or medium gateways are useful for the short or mid term, buying us some time, but this is not something we want for the long term.

And this motion is for rather the long term as the one from jl or cybnate or nagalim, i understand.

So i would like to see either an upper limit in the spread of gateways and/or a limited period in which we allow for large spreads. Both would be ideal

This way it would make us work hard on trying to get a lot of reserves so we can provide always and only a below 1% spread liquidity or some kind of gurantee that we will never pass a certain limit in gateways spread (like 5%).

Of course not!

And to provide them with sufficient supply, I created two tx to deposit 20k NBT now and 65k NBT on demand to gateways.

This is not about using only large spreads.

The proposal deals with <1% spread for ALP and MLP and above 1% only for gateways.

Of course we need them as the last line of defence they are now, mid-term and long-term!

And now mid-term and long-term liquidity at <1% spread would be welcome.

If that liquidity fails, gateways kick in.

You don’t know how dire situations can get.

I have a feeling what offset is ok for now. It sufficed to get the peg defended at the line it is.

I wouldn’t dare putting an upper limit there.

That limit needs to be set market aware.

Don’t try to limit of what you have no idea.

After careful consideration, I have decided I will add this motion to my date feeds.

The reason is that we do not have the means right now to provide liquidity (funded by Nu) at only a tight spread at all time.

The main reason being that we do not have enough BTC reserves compared to the trade volume.

I think in the future, we want to reduce the ratio (reserve/outstanding nubits) while at the same time increase the ratio (reserve/nubits trade volume).

That way we can make more profits while at the same time ensuring that we can exchange more nubits for bitcoins at any time.

ALP/MLP will continue to operate at spread <=1% in this motion.

Spreads higher than 1% have been used at least twice in a crucial way once in Jan this year and a second time just now, tks to the work of @masterOfDisaster .

They have been quite useful in protecting the peg without downgrading it too much (we have had up to 0.97 usd on coin market cap)

So I think this motion is important for the time being and is a temporary measure.

The idea is to use it a few months, buying us some time, to increase the demand for NuBits drastically and replenish the buy side. Then, ideally we will design better liquidity provision schemes that will make sure that the vast majority of liquidity is provided at a spread <= 1% with a large volume .

The reserve ratio needs to be increased, if the reliability of NBT shall be increased.

A low ratio of reserves/“NBT in circulation” had a part in bringing us where we are now.

Right. But this is not the last step in the evolution. It was just the most important step right now to provide an alternative for the errant versions of Jordan and Cybnate.

tl;dr (will be the conclusion of this post as well): The economically improved approach is market awareness, or more precisely: market aware offsets combined with parametric order books for all pairs, except NBT/USD.

I believe <1% spread is not the optimum for all situations.

The vast majority of liquidity needs to be provided at a reasonable spread, which is not necessarily 1%.

For NBT/USD it’s differnet and quite simple. That’s because NBT is pegged to USD.

But it isn’t pegged to BTC or USD quoted in BTC. This is a synthetic peg, that needs to be treated differently.

Parametric order books are as important as market awareness for the spread of trading pairs other than NBT/USD.

I hope that during most times we can offer a lot of liquidity at a spread below 1% for non NBT/USD.

We should only guarantee a tight spread for NBT/USD, though!

For other pairs, e.g. NBT/BTC, a tight spread with symmetric offsets is only good for non-volatile BTC times.

As soon as BTC starts to get volatile, the spread must increase.

If BTC is bullish, you need an increased buyside offset, while the sellside offset can stay low.

If BTC is bearish, you need an increased sellside offset, while the buyside offset can stay low.

You achieve that by making the offset a function of the size of one side.

This way it doesn’t matter, if funds get traded, or orders pulled.

The orders that remain, remain at an increased offset.

It’s wishful thinking that you can provide a tight spread at all times.

It’s too expensive to do that.

It’s not sustainable.

And even with 100% reserve it wouldn’t be reliable without a lot of efforts and schemes to allow it.

To make an extreme example:

let people buy 100,000 NBT at a BTC rate of $100. Keep the 1,000 BTC on reserve.

They keep the NBT until BTC drops at $50. Then they start buying BTC. After Nu received 50,000 NBT back, the BTC reserve is empty.

What do you do with the outstanding 50,000 NBT, that people want to trade for BTC?

This example is extreme, but it shows that schemes like NuSafe need to be an even more important part of the reserve scheme.

That way, Nu wouldn’t keep the 1,000 BTC, but keep them as $100,000.

Remember, “NuBits - always a Dollar!”?

This way it works to keep a full reserve, but costs money to operate NuSafe and alike. The reliability of the 100% reserve scheme is in danger again.

As yourself: would you as a (future) NBT holder rather always have the option to trade your NBT for, say BTC?

Even if that means paying an increased offset?

Or would you want to live with the risk of being too late and being stuck with NBT?

We shouldn’t overly focus on daytraders, who do high frequency trading. They might not create as much demand for NBT as we hope they do. They can do a lot of trades with a fistful of NBT.

We should focus on people who buy NBT now, knowing they are a reliable store of value (quoted in USD), while they can be handled like a crypto currency, and aren’t afraid to hold them. They can hedge long-term, keeping the demand for NBT high.

The daytraders require a tight spread to do their business. All other don’t.

A related discussion is dealing with inflation free currencies. I don’t want to mix it in here, although I perceive it as a very important sales pitch for long-term hodlers.

I want to focus on a sound, reliable, reasonable liquidity provision scheme here.

The economically improved approach is market awareness, or more precisely: market aware offsets combined with parametric order books for all pairs, except NBT/USD.

Here’s a start for creating formulas: